Using the Kelly Criterion to Maximize Investment Profits: A Practical Guide

The Best Investment Deserves The Largest Exposure - Marc De Mesel *****Introduction***** When an investor puts his or her money in the market, their aim is to make as much money as possible at the lowest level of risk. You might think "I am not an investor, I don't have much money". In reality, most of us are investors, one way or another. Whether it is putting down the deposit for your first car, the lease for your apartment, or whether to buy more Bitcoin Cash in addition to what you earned on read.cash or buy some Ethereum instead, you are making investment decisions in various sizes. There is one question smart investors ask themselves every time they are about to make an investment decision. Is the amount I am allocating and committing to this investment too large? Too small? Can I afford the size of this bet? Will I regret it later? You might wonder if there was a framework or a criterion that one could use to get these answers. It turns out there is. We just need to focus on the question we want to answer. If we want to maximize the long-term growth rate of wealth, one of the answers (actually, the scientifically tested best answer) is **optimizing the bet size** using the Kelly criterion. Kelly criterion is a mathematical formula for investment position sizing. It helps you determine the percentage of your capital you should bet on any given circumstance, **assuming you have an advantage**. The goal of the equation is this: **don’t go broke.** **Kelly’s criterion**, Kelly’s formula, Kelly’s bet and Kelly’s strategy all refer to the paper written by John L. Kelly, Jr. in 1956 that explored the relationship between the rate of growth of wealth and bet size. Kelly was an American scientist who worked as a researcher at AT&T’s Bell Labs. He originally developed the formula to help the company with its long-distance telephone signal noise issues. Later, it was picked up upon by the betting community, who realized its value as an optimal betting system since it would allow gamblers to maximize the size of their earnings. Kelly criterion typically leads to **higher wealth in the long run** compared to other types of strategies. https://www.princeton.edu/~wbialek/rome/refs/kelly_56.pdf Although it was reported that Kelly never used his formula for personal gain, it is still quite popular today and is used as a general money management system for investing. The Kelly capital growth strategy has been used successfully by many prominent investors, such as **Warren Buffet** of Berkshire Hathaway, and **Marc De Mesel** who quotes the Kelly criterion in his videos and shares his estimates and Kelly calculations of his investment portfolio in a spreadsheet format. You can find those spreadsheets labeled as "Crypto Investment Plan" in the description section of some of his Youtube videos. One might wonder what a criterion focused on betting and gambling has to do with investing. The answer is that, after researching an investment decision, it becomes a decision with inherent risk and a lot of unknowns, just like gambling. I might dislike gambling and the notion that I am gambling with my money, but whether I am buying a house, investing in gold, or in Apple company stock, I am exposed to various types of **risk** (weather, economy, currency exchange rates, wars, pancemics, etc.). That is why, the term "bet size" is also used to refer to investment position size. *****How do you determine the size of your bet?*****

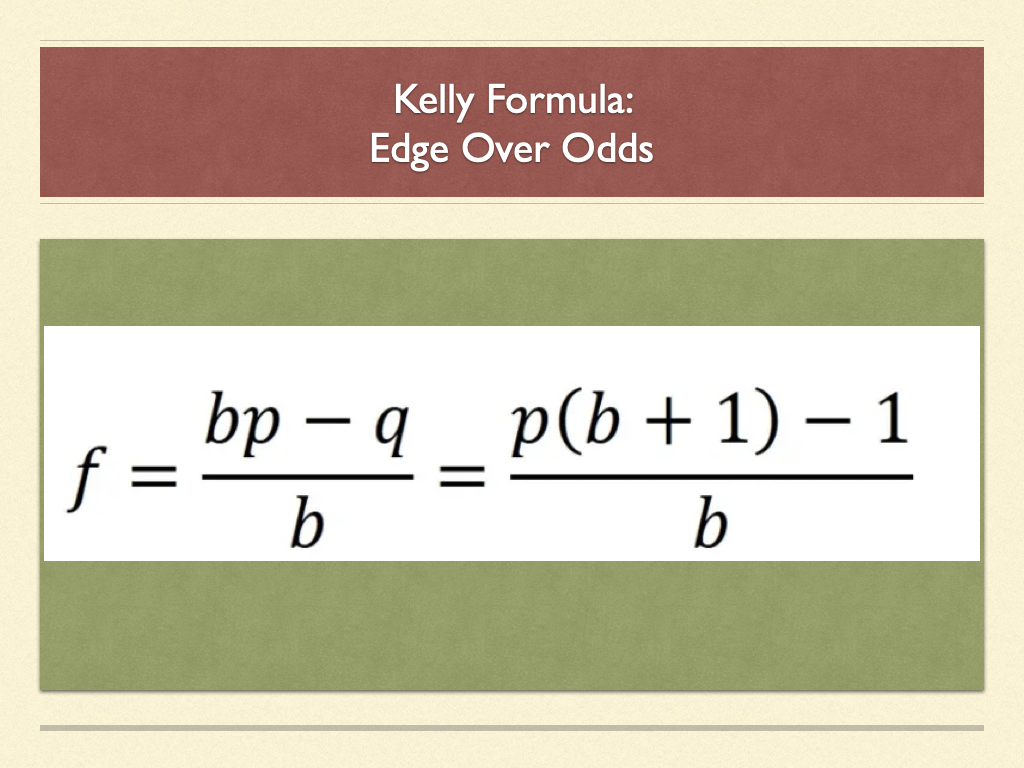

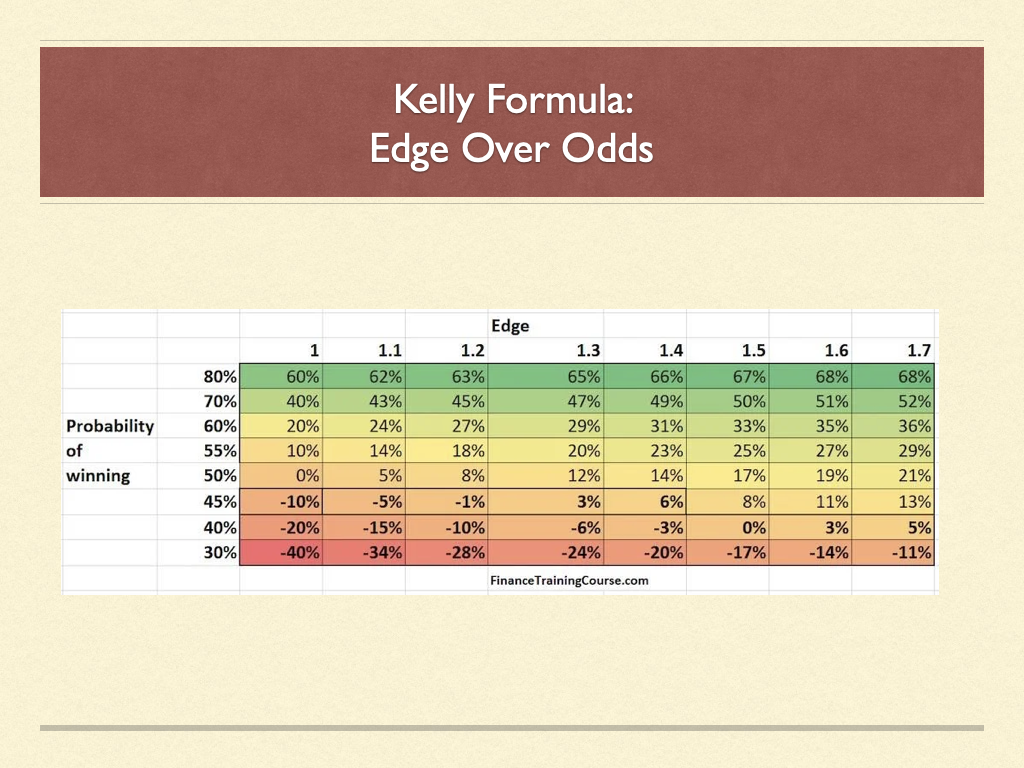

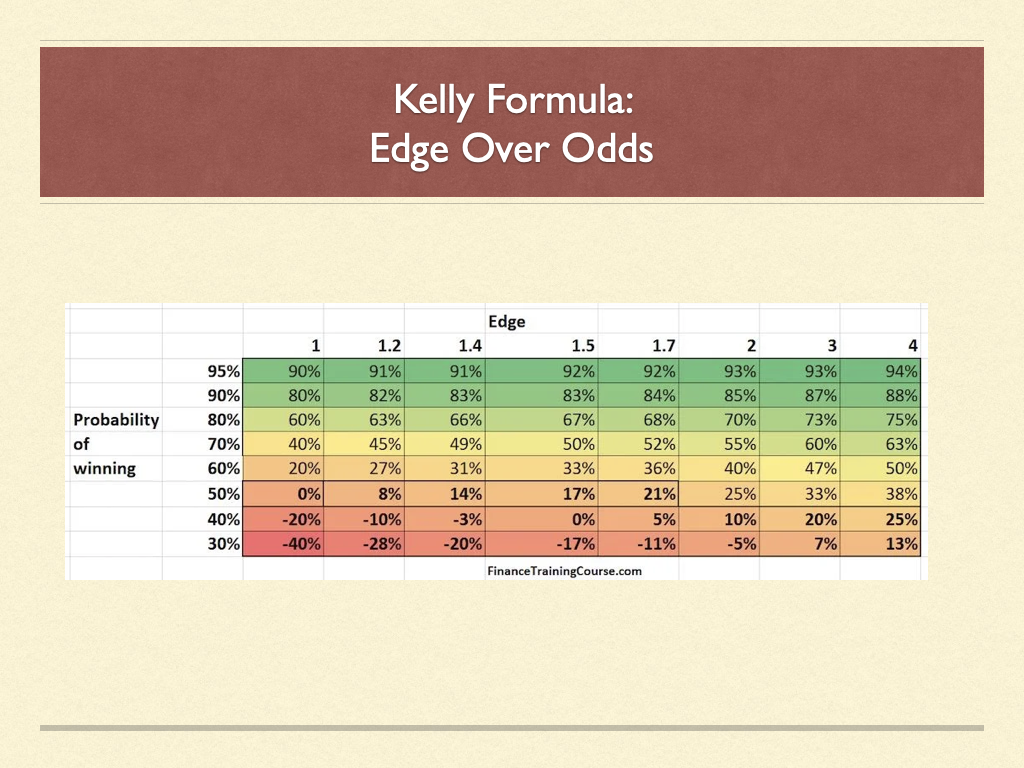

If you, like me, can get intimidated by math equations, don't worry; no more math after this point! The Kelly criterion can be simplified as: ***Edge / Odds = Fraction of capital that should be allocated*** The edge is the amount you are likely to win (on average over multiple bets). The odds are the assessment or likelihood of that win. How would optimal bet sizes vary with changes in the probability of winning and edge? If the odd were in your favor (80% chance of winning) and your edge stood at 1.2, should you bet the entire bank or only part of your capital? The table below presents optimal bet sizes based on Kelly for changing values of edge and odds. The vertical index lists a scale of probabilities that goes from high to low as we move from top to bottom. These figures represent the probability of winning the bet. the horizontal index lists increasing edge as we move from left to right. The numbers listed in the table represent estimated bet sizes using Kelly’s criterion for each cell. For instance with a **60%** probability of winning and **1.5** edge, the recommended Kelly’s criterion bet is **33%** of your investment capital.

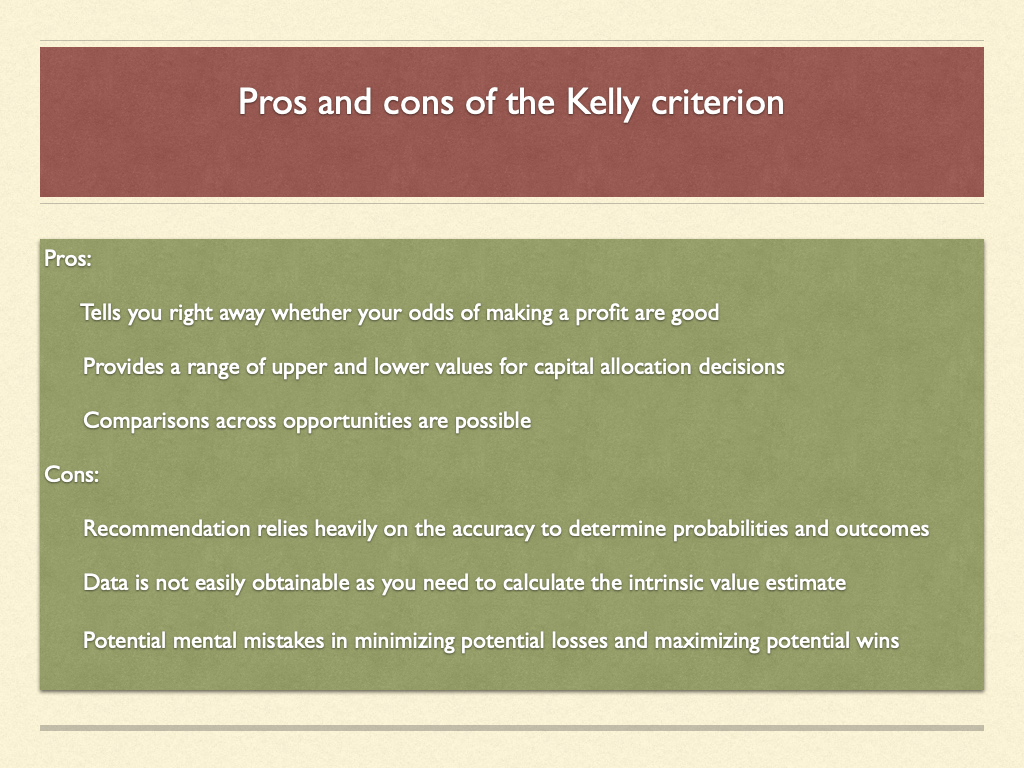

The color coding shows areas of strong promise (**shades of green**), neutral (**between lime green and yellow**) and unfavorable (**ocher and hints of red to red**). Even the best odds (**80% chance of winning**) and a reasonable edge (**1.4**) lead to a bet size of **2/3 of your capital**. Remember under Kelly the objective is to not maximize expected payoff but growth in capital. Growth in capital over multiple bets or seasons has a central condition: survival. If you have nothing left to bet, if you have depleted your capital, you are out of the game. The next time you come across a sure thing, you know what to do. Hold a part of your capital back, don’t bet the boat. Capital preservation, not accumulation is the key to maximizing wealth over a multi-period investing time horizon. What dominates the determination of bet size? **Is it the probability of winning (your odds) or the pay off (your edge)?**

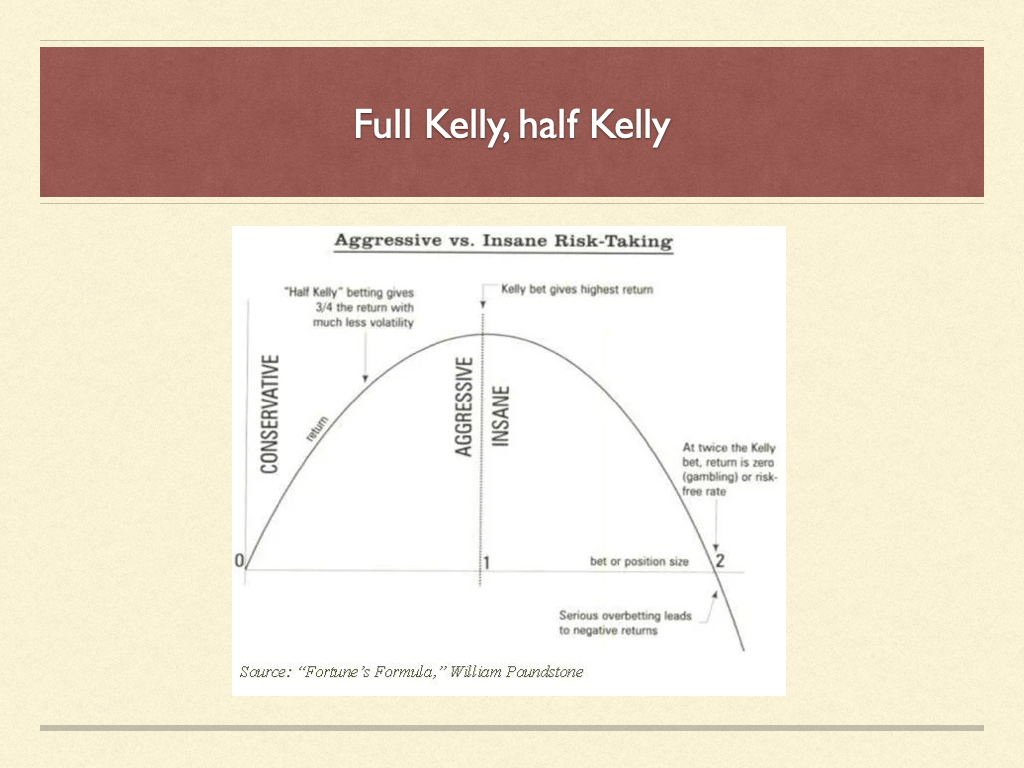

The answer is that the **probability of winning** is much more important than the edge. If you look at Table 2 above, you will notice that at higher probabilities of winning, an increase in payoff will only result in a slight increase in your bet size. Kelly is not going to recommend that you bet all your money. The model would still suggest that you hold some capital back. Again, the goal is: **don’t go broke.** OK, let's see this strategy at work. *****Putting It to Use***** Frequent traders can easily put Kelly's system to use. If you are a trader, you can follow these simple steps: The Kelly criterion is based on your previous trades. Access your last 50 to 60 trades. You can do this by simply asking your broker or by checking your recent tax returns if you claimed all your trades. If you are a more advanced trader with a developed trading system, simply backtest the system and take those results. The Kelly criterion assumes, however, that you trade the same way now that you traded in the past. Calculate "W"—the winning probability: To do this, divide the number of trades that returned a positive amount by your total number of trades (both positive and negative). This number is better as it gets closer to one. Any number above 0.50 is good. Calculate "R"—the win/loss ratio: Do this by dividing the average gain of the positive trades by the average loss of the negative trades. You should have a number greater than one if your average gains are greater than your average losses. A result of less than one is manageable as long as the number of losing trades remains small. Input these numbers into a **Kelly's equation calculator**. You can find a few of them online. I like the one here: **dqydj.com/kelly-criterion-bet-calculator/** https://dqydj.com/kelly-criterion-bet-calculator/ Record the Kelly percentage that the equation returns. This is the percentage of your capital the Kelly criterion is recommending to invest. The above is straightforward for frequent traders since they have a long hisotry of hundreds of trades. It is more challenging for investors, but they can still use the Kelly criterion to optimize returns. An investor just has to use estimates rather than exact calculations for the edge and odds. *****A practical example: Ethereum***** Suppose you did your research and you think that **Ethereum** is going to increase to **5 times** its current price. You estimate the probability of this happening to be **70 percent**. You use the online calculator mentioned above. You put 0.7 in the probability field (70%). You enter 5 in the "odds" field. You calculate and get **64%**. Kelly criterion recommends that you allocate 64% of your capital to this trade for optimal growth. https://dqydj.com/kelly-criterion-bet-calculator/ ***Full Kelly, fractional Kelly and rebalancing*** Just because Kelly suggests that you should bet 64% of your pool of capital, should you? The answer is no. Your estimates of odds and edge are most likely inaccurate and off. While the Kelly strategy will outperform all other strategies over time, the required time duration for Kelly to outperform may surprise you. Depending on the value of parameters that define your market and your bet, the time required for Kelly to outperform all other strategies with a certain degree of confidence may range anywhere from **80 years to 200 years**. With shorter time frames, randomness and risks can be more exaggerated, so a more conservative approach is wise. Which brings us to fractional Kelly strategies. Models that don’t be the entire amount recommended by Kelly but some fraction. There are different opinions on how effective this approach is, but there is consensus that a fractional Kelly approach leads to lower short term risk at the cost of giving up potential upside. In other words, fractional Kelly strategies provide more security (less risk) but with less growth.

So for the above example with Ethereum, you might want to use **half Kelly**, or **32%** of your investment capital on that trade for a more conservative approach. A second element is **rebalancing** and fixed portfolio weights: Your original strategy and allocated weights go out of alignment as soon as any one position outperforms the others. You may want to regularly review your investments and rebalance your positions (adjust actual dollar value by buying and selling) to get the weights back in alignment. This helps with performance over a multi-period investment horizon but adds to transaction and execution costs. Despite these costs, rebalancing leads to better performance when compared to strategies without rebalancing.

*****Summary***** The Kelly Criterion is a money management tool that helps you calculate how much money you can afford to risk on each new trading position. It calculates a Kelly percentage number based on how much profit or loss you have made on similar trades in the past, or based on your estimates of edge and odds. This number tells you what percentage of your trading account you could sensibly risk on this kind of trade now. Market conditions will affect the outcome of any trade, so make sure that you only include in your calculation trades that were taken during similar market conditions as those in effect now. Do not over-rely on the Kelly criterion to judge position sizes and risk tolerance. Whatever it tells you, never risk more than your usual maximum risk level. Consider using fractional Kelly calculations. That is all. I hope this was a useful introduction to the principles of the Kelly criterion. There is a lot more details related to this strategy, with advanced concepts and complicated math. But what I personally like about the Kelly strategy is that it can be used by anyone to help with the investment position size determination. You can use an online calculator, enter your estimates of the probability and odds, and calculate the Kelly percentage. You can then take a fraction of that result, according to your level of risk tolerance, and allocate that much percentage of your money to your desired investment. **Thank you for reading!** *****References and Recommended Further Reading***** Calculator: **dqydj.com/kelly-criterion-bet-calculator/** https://dqydj.com/kelly-criterion-bet-calculator/ https://financetrainingcourse.com/education/2019/10/kelly-criterion-founders-startups-optimal-betsize/ The Kelly’s Criterion in Blackjack, sports betting and the stock market, Ed Thorp, 2007 – https://wayback.archive-it.org/all/20090320125959/http://www.edwardothorp.com/sitebuildercontent/sitebuilderfiles/KellyCriterion2007.pdf https://demonetizedblog.com/2019/02/23/edge-over-odds/ http://home.williampoundstone.net/Kelly.htm The Dhandho Investor: The Low-Risk Value Method to High Returns. 1st Edition.

9 comments

Really good evening read ! Remembered using this when playing roulette!

glad you enjoyed it!

I have not yet finished reading it, but I can already tell it's a very impressive article. 👍

thank you!

Very interesting Omar, thank you. Would like to learn more about rebalancing part at end. Is it really true it improves performance over longer period? Should one not hold a 100 bagger until it 100 bags? Confused.

Thank you so much Marc for reading and for the generous tip! Regarding rebalancing, it is certainly confusing. Most of the resources discussing the Kelly criterion recommend it, and claim that it leads to higher returns in the long-run. This is based on research papers studying rebalancing and its optimal frequency using mathematical models and scientific simulation (Monte Carlo simulation, etc.). Here are some examples: 1. Practical Implementation of the Kelly Criterion: Optimal Growth Rate, Number of Trades, and Rebalancing Frequency for Equity Portfolios: https://www.frontiersin.org/articles/10.3389/fams.2020.577050/full 2. Application of the Kelly Criterion on a Self-Financing Trading Portfolio: https://core.ac.uk/download/pdf/85145338.pdf 3. Rebalancing Frequency Considerations for Kelly-Optimal Stock Portfolios in a Control-Theoretic Framework: https://www.researchgate.net/publication/330585357_Rebalancing_Frequency_Considerations_for_Kelly-Optimal_Stock_Portfolios_in_a_Control-Theoretic_Framework Digging deeper, however, one can notice the following points: 1. No agreement on the recommended rebalancing frequency. 2. Less frequent rebalancing is generally recommended (e.g. quarterly). More frequent rebalancing can be counterproductive, leading to what is called Proebsting’s paradox: https://en.wikipedia.org/wiki/Proebsting%27s_paradox 3. Most of this research was done on equity / stock markets, where the typical return is at most a few hundred percent per year. 100 baggers are unusual there, unlike in crypto. 4. I guess the above point is crucial, since the different expected returns and time-frames are important variables. Could the nature of the asset also affect the results in other ways? I don't know. I think the best application of a scientific tool like the Kelly criterion, is to combine it with intuition, especially if you are using a conservative approach (fractional Kelly). I say you can’t argue with 50% CAGR :) Let those profits run!

Wow! Applying Mathematics solving feature here is awesome. I am a math major but I kinda find it hard though. I will try to re-read it again. You did a great article here sir. ☺️

thank you very much @Zhyne06

Thank you for the upvote sir ☺️