The Tricks Your Mind Plays On You: 20 Biases That Impact Your Investment Success (Part 1/3)

*"The investor’s chief problem - and even his worst enemy - is likely to be himself."* *Benjamin Graham, The Intelligent Investor.* - ***Introduction*** Hello readers! We don't always see things as they are. We don't simply glean information through the senses and act on it. Instead, our minds give that information their own spin, which can sometimes be deceptive. The inner experience is not always in perfect sync with what is going on in the outer world. There are some alarmingly standard mistakes that people make again and again. These common thinking errors that hinder our rational decision-making are called “biases”. Several biases have been described. It is very easy in the heat of the moment, or when subject to stress or temptation, to fall into one of these mind traps. Behavioral finance studies these biases which can negatively affect investor's returns. There are two categories of biases: cognitive bias and emotional bias. Cognitive biases involve basing decisions on established concepts that may or may not be true. Emotional biases are often spontaneous. They involve basing decisions on individual feelings. The bad news is that we can't get rid of cognitive and emotional biases. The good news? The better we understand them, the more often we can subvert them—or even leverage them for our own benefit. The first step toward overcoming biases is to acknowledge that we have them. The most sophisticated thinkers fall prey to their own cognitive biases, so at least we're in good company. The second step is to take advantage of tools that can help balance out our own irrational tendencies. Wise investors can limit the potential impact of behavioral biases by developing and focusing on their own systematic investment process (what to invest in, position sizing e.g. using Kelly criterion, when to sell, etc.). There are also recommendations specific to each type of bias to help avoid or overcome them. In this 3 part series, I will go over 20 common traps / biases / fallacies that we face, and discuss how to outsmart them. I hope that this series will help the reader make better decisions, in investing and in life.

Let’s dive right in. ***1. Confirmation Bias:*** **What is it?** Once we make a decision, we want to be right, so we tend to block out information that might show we’ve made a mistake and pay attention only to data points that make us look smart. The confirmation bias is the tendency to seek information that confirms or favors your pre-existing belief or hypothesis, and to reject or trivialize any suggestion that disagrees with it. When we become attached to our beliefs, we're really good at spotting facts that seem to support them. After all, it's easier to convince ourselves we're right than it is to consider another view. All too often we feel more confident regarding a potential investment when we read comments by experts or other investors which validate, or confirm, our hypothesis and reasoning for investing in a company or cryptocurrency. Investors often watch financial news networks or read investment blogs, looking for individuals who lay out the same hypothesis they have regarding the stock or cryptocurrency and thus validating their basis for investment. Confirmation bias is a basic human flaw: **We like to think we're always right**, and will go to great lengths to seek out information to uphold our preconceived notions. **Why avoid confirmation bias?** The problem with confirmation bias is that when we refuse to take in conflicting information, we filter out important data that could help us make more informed decisions. For example, you may get a "hot tip" about a company and focus on all the good news you read, while ignoring the bad news. Or when you identify a trading signal: You will notice the technical indicators which support your opinion, and not those against it. **Any bad idea can look good if you want it to work**. The confirmation bias can have a really dangerous effect when investing. Investors will have a partial picture of a situation because of confirmation bias. Because of one-sided information which biases our frame of reference, we are prone to making flawed decisions. Confirmation bias can enhance potential negative effects of other biases such as overconfidence, as we tend to believe the more “facts” we read and review, which often agree or relate to our view of the investment thesis, causes higher levels of conviction. This can lead to investors buying outsized positions or taking on excessive risk, as they believe the facts they have reviewed, which often simply validate their view, suggest an even higher level of conviction in any investment is justified or warranted.

**How to avoid confirmation bias?** Investors should spend almost zero time in their investment process looking for confirmation of their thesis, but instead focus on **disproving their thesis** and understanding what in their views could be wrong and cause an alternative outcome to the one they believe is most certain. Unfortunately, investors are twice as likely to look for information that agrees with their thesis than they are to seek out disconfirming evidence. When everything seems to support your market view or reinforcing your idea, stop! Reflect further and seek for reasons against your view. This can save you from slipping into the pit of over-confidence. **Seek out information that goes against your pre-existing beliefs**. If you think a project will succeed, go out of your way to brainstorm reasons it might not. Brainstorm. If possible, have three potential hypothesis instead of one. Do not rationalize conflicting evidence Say for instance that you are looking for a stock that is friendly to the environment. At the same time, you have been looking at an oil company that has performed well lately. You start researching if this oil company is green. Then you come across an article saying that the company is ‘thinking’ about investing in solar panels. “Yes!”, this was exactly what you were looking for. The hypothesis was that this company was environmentally-friendly. Once you found an article “confirming” this, you stopped searching for more information. So you now have only information that confirms what you wanted. The most valuable research would actually be the opposite. **You will do better research if you try to break your hypothesis**. Try to find out if the company is an enemy of the environment. If you can't prove that, the investment is good (if you regard green investments as a goal). The strength of many of history’s most accomplished scientists has been their ability to overcome their confirmation bias and to see all sides of a problem. Carl Jacobi, a famous 19th century mathematician, said: “**Invert, always invert.**”

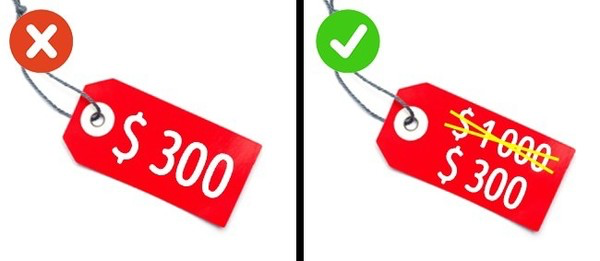

***2. Anchoring Trap:*** The anchoring effect is the tendency to privilege the first information we encounter, even when subsequent information turns out to be more relevant or realistic. Anchoring is a phenomenon where someone values an initial piece of information too much to make subsequent judgments. For example, if you first see a T-shirt that costs $1,000 – then see a second one that costs $200 – you're prone to see the second shirt as cheap, even though both are really expensive. People often take decisions based on the first piece of information they receive and stick to it. No matter what research says or how hard you try to convince them, nothing can change their opinion. This tendency to come to a decision based on the first bit of information you have is called anchoring bias. That is why, in salary negotiations, it is recommended that you be the first to say a number: according to the anchoring effect, you've now set the expectations for the rest of the discussion. An investment example is the electronics retailer Radio Shack. Once a thriving seller of personal electronics and gadgets in the 1990s, the chain was crushed by online retailers such as Amazon. Those trapped in the perception that Radio Shack was there to stay lost a lot of money as the company filed for bankruptcy and closed most of its stores. Another example of this is holding on to the narrative that BTC is a good long-term store of value, and ignoring the fact that since 2017 it has become a failed coin with no utility.

**Why it is a problem:** The anchoring bias makes you get “hung up” in a piece of information you are given. This may make it hard to change your mind if new information is made available. Charles Darwin said "It is not the strongest of the species that survives, nor the most intelligent that survives. It is the one that is most adaptable to change." If your mind is anchored, you will have a hard time adapting. Since many investment decisions require multiple complex judgments, they're vulnerable to anchoring bias. Looking at past history can be a distraction. For example, a person may hold on to a stock longer than they should because they've "anchored" on the higher price that they bought it at. The buying price biases their judgments about the stock's true value. **How to avoid anchoring bias?** In order to avoid this trap, you need to remain flexible in your thinking and open to new sources of information, while understanding the reality that any company can be here today and gone tomorrow. Before investing your money based on the first piece of information that you get, try to counter question the fact. Put your own research to analyze if this information is even relevant to your investment objective. Sometimes you have to stop looking at past history, and assume it hasn't happened! Take time to do research and make a decision. A comprehensive assessment of an asset's price helps reduce anchoring bias. Finally, be open to new information even if it doesn't necessarily align with what you've initially learned.

***3. Hindsight Bias:*** The hindsight bias is when you view an event that has happened as more predictable than it was. Hindsight bias is the misconception, after the fact, that one “always knew” that they were right. Hindsight bias is a psychological phenomenon in which one becomes convinced that one accurately predicted an event before it occurred. Consider the 2008 financial crisis or the dot-com bubble of the late 1990s. If you talk to many people now, they may state that all the signs were there and everyone knew it was coming. However, if you examine the history, you learn that analysts or investment professionals who were screaming that there was a problem at the time weren’t listened to, in fact, they were laughed at and investors largely ignored their warnings. If it was so obvious why did it happen and why did it affect so many people? Why didn’t all the people claiming that it was obvious short the market and become very rich?

**Why is it a problem?** The danger of this bias is to take too many risks because you expect to see what is coming next time because the last event was so obvious. It causes overconfidence in one's ability to predict other future events. Hindsight bias prevents us from recognizing and learning from our mistakes. We talk about it as a limit to our learning because we tend to believe after the fact that we knew about something all along. **How can we deal with hindsight bias?** 1. First, remind yourself that you can't predict the future. 2. Examine the data. 3. Record your thought process. Hindsight bias is revisionary. 4. Consider alternative outcomes. Make sure to list these, too. 5. Make your decision. 6. Analyze the outcome. 7. Use an investment diary, comparing outcomes to the reasoning behind our investment decisions, is a good way to keep this hindsight bias in check.

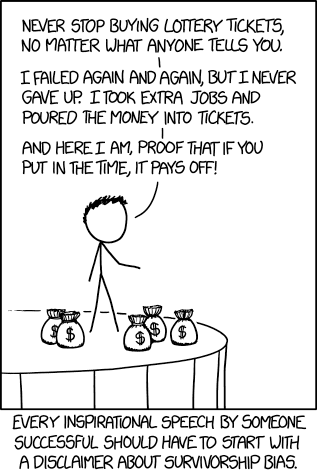

***4. Survivorship Bias:*** Survivorship bias or survival bias is the logical error of concentrating on the people or things that made it past some selection process and overlooking those that did not, typically because of their lack of visibility. People tend to focus on these survivors, even if they survived in large part due to **luck rather than viability**. For example, a gym might feature those who have toned up quickly as a result of going to their facilities. But, of course, what they never show is those who signed up but achieved no more than a depleted bank account! Survivorship bias comes into play when a person starts with a success story, whether it be a successful entrepreneur, a world-champion athlete or a billionaire stock investor, and attempts to reverse-engineer a personal pathway to similar success. The presumption is if I do exactly what this billionaire investor or entrepreneur did, I will be a success just like he or she was. In reality, the most successful outliers on Wall Street over any given short-term period almost always took some extreme amount of risk that just happened to pay off big. But just because a particular strategy worked one time for one person does not mean it is a good strategy for others. The most common place you will find this bias is in investment courses, webinars, and consultancies. They often use it as a sales trick, disguised as “Check our cases of success”. **Nobody shows examples of failure.** Survivorship bias is best summed up as "**dead men don't tell tales**."

***5. Mental Accounting:*** Mental accounting, also known as "**two-pocket**" theory, is the concept of giving money different value depending on the source. It is where people treat money differently depending on where it came from and what we think it should be used for. Would you say that $500 from X is worth more than $500 from Y? No, probably not. You don’t know what X and Y are, and $500 is therefore worth the same to you. What if I say that X is your salary and Y is from a large work bonus? Would you be more likely to spend the $500 from the unexpected bonus on some unnecessary luxury items? Yes, that is more likely. But should it be like that? No, whatever the sources are, you have a total of $1,000 and that is what you should take into consideration when deciding what to do with the money. The idea is that we separate our money into "**mental accounts**" for different uses, which influences our spending decisions. We guard some money cautiously when we mentally categorize it for a house, but spend it liberally when it's "fun money”. Another example of mental accounting is people's willingness to pay more for goods when using credit cards than if they are paying with cash. **Why is mental accounting a problem?** Mental accounting can sometimes hurt your bottom line. It can confuse your financial priorities. For example, investors are, as a group, highly prone to the “money you can afford to lose” variant of mental accounting. Under this notion, investors view some arbitrary amount of their investment capital as “play money” which they feel comfortable squandering on speculative and uncertain things. At first glance, this appears to be a sensible decision-making. It seems prudent to clearly delineate between money that matters and money that doesn’t. The problem, of course, is that “money you can afford to lose” is a purely mental creation. **How to overcome mental accounting:** Stop keeping everything in your mind and write it down. Create a **budget** to guide your financial decisions and better determine when to save versus spend money. And create a plan for how to spend windfall gains, like an inheritance or work bonus, ahead of time.

- In Part 2 and Part 3 of this series, we will continue going through the rest of 20 selected types of biases. Stay tuned, and please be alert to these biases in your life and investment decisions! https://read.cash/@Omar/the-tricks-your-mind-plays-on-you-20-biases-that-impact-your-investment-success-part-23-f04e8c31 https://read.cash/@Omar/the-tricks-your-mind-plays-on-you-20-biases-that-impact-your-investment-success-part-33-77a6a688 Thank you for reading. Feedback is much appreciated. - Omar

10 comments

Cognitive and emotional biases. Indeed informative! New learnings to me. Worth reading!

thank you!

"dead men don't tell tales" this is a bitter truth i think. And the points you have written under How can we deal with hindsight bias? I think this way a bit. Found the article very useful. Atleast my time isn't wasted reading it 😊

thank you for reading..

I would love to hear more from these biases about investors. All I know is being bias in judging people,but upon reading on, I find new knowledge from it... Carry on. 😊

Yeah often times I do mental accounting and I keep losing all the numbers on my mind. So I decided to buy a small notebook to monitor my expenses. It helps. Awesome article to read :)

An entertaining article, I learned a lot of new things, but I also learned myself in some points. Especially I often encounter the phenomenon of "Hindsight bias". Indeed, you should not deceive yourself, no one can predict the future for sure.

"We like to think we're always right" True, sometimes when we think of something and for us it was right, we're deaf of other's opinion or suggestions. I am sometimes bias with things and sometimes with people. But now, when I enter the crypto world, I sometimes have biases in other coins. Sometimes also, I like the coin now but when it went down I transfer to other coin.😅 Sometimes what I think was right was truely wrong. 😅

I've noticed that survivorship bias is used to gaslight people into sticking with bad jobs. The supervisor will say, "If you keep hammering away at these rocks all day, you'll advance in the company and all your dreams will come true. Keep smashing those rocks and don't stop." I see any signs of survivorship bias as a red flag.

Again, this is a very informative post. I happen to read the third part first. Hehe. This is very helpful for me since I want to develop a strategy on how to handle my BCH earnings