We covered the first steps towards Crypto trading antifragility in part 1: downside with its risks identified and characterized, then some recommended approaches around those risks. Now we are going to cover the upside portion of convexity via an approach seldom used in this space.

There are several ways to achieve a theoretically unlimited upside in crypto, the most common and main business of big exchanges is altcoin trading. Future contracts, another common way, became popular during the 2017 market hype, especially on BitMEX. The advantages of futures are the added possibility of making profits with price drops, and the use of high leverage.

But for this post I’m going to scratch the surface of Crypto Options on Deribit. Options offer so many possibilities of complex strategies that they can become intimidating for beginners – one of the reasons why they are very niche compared to alts and simple futures. But just a superficial understanding combined with the risks we covered before can result in massive profits, even more so when there is blood on the streets.

For instance, during the ‘Crypto Black Thursday’ on March 12 a few options contracts had gains of 500X in BTC value; the lucky ones who bought at the minimal price could have made 1000X or more.

A few days before the crash it was possible to buy a Put option contract, way out of the money, for 0.001 BTC, the same contract was worth 0.5 BTC when everyone was desperate during the free fall.

We’ll cover all the jargon soon, but first...

What Is An Options Contract?

Like futures contracts, options are derivatives, their value is derived from an underlying asset. In our case it could be either BTC or ETH (at the moment).

A futures contract is simply an agreement to buy or sell the underlying asset in the future. In the crypto space, the time factor is not so important due to the innovation of perpetual contracts. As long as you are willing to pay the funding fees, there is no need to worry about the expiration, so you can make a simple directional trade, either up or down, regardless of timing.

In options, however, by definition this limitless expiration is not possible because they are simply a contract (or agreement) to buy or sell an asset at a specific price and date in the future. At expiration, if the contract is worth something, you can receive the underlying asset. Until then, you can trade the contract at will [1].

The buyer of an option pays to receive a right, the seller receives money to give up a right and have an obligation instead.

There are two types of options, Calls and Puts.

A Call is a contract to buy the underlying asset in the future.

Let’s say, for instance, you find a house you want to buy. The current price is 1.000.000USD, you are quite sure you’ll buy it, but first you need to convince your significant other this is a good investment. The convincing might take some time, and to reduce the risk of someone else snatching the place, you propose the seller to hold off the sell for one month. For his trouble of taking the house off the market in this period, you’ll pay 10.000USD. This agreement is a Call option, you pay to have a right to buy, while the seller receives money to have the obligation of taking the house off the market.

A Put is the exact opposite, a contract to sell the underlying asset in the future.

Imagine you’ve just bought your Lambo during a big bull market, since lots of precious crypto were spent, you mitigate your risk buying an insurance policy for one year. If something bad happens in this period, like the car getting “Rekt” or stolen you get its value back.

The insurance contract is like a Put option, you pay for the right to sell the asset at a predetermined price, and the insurance company receives the money for an obligation to buy.

These examples are simple illustrations about the basics behind Calls and Puts. There are more variables in play in the options market, which will determine how they are priced and traded.

Two crucial aspects to keep in mind about these simple buy or sell operations are:

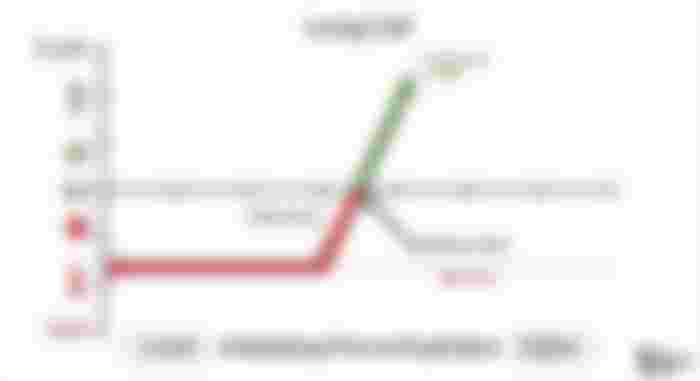

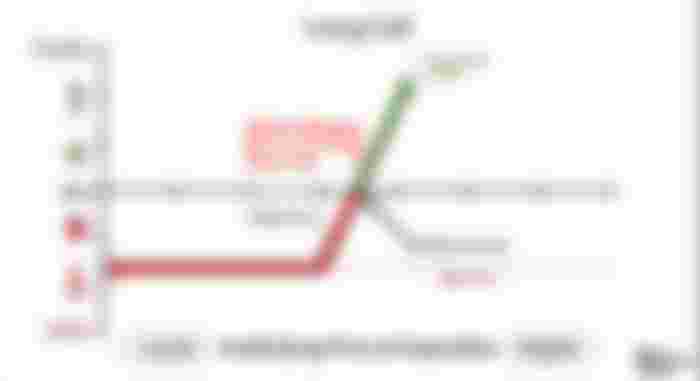

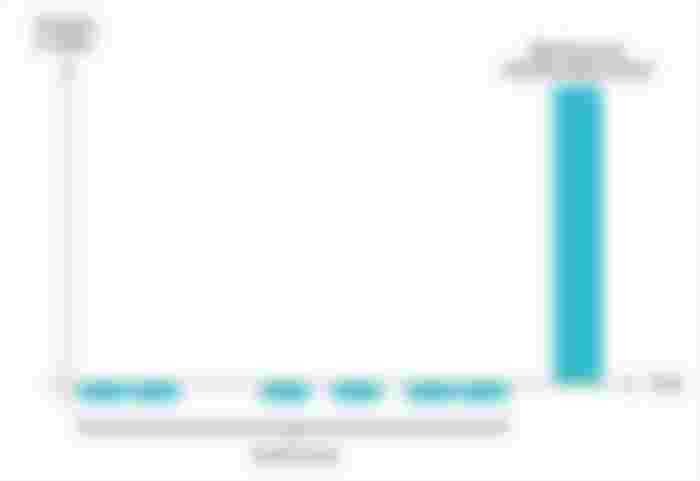

The buyer has a convex position, because his losses are limited and gains are theoretically unlimited.

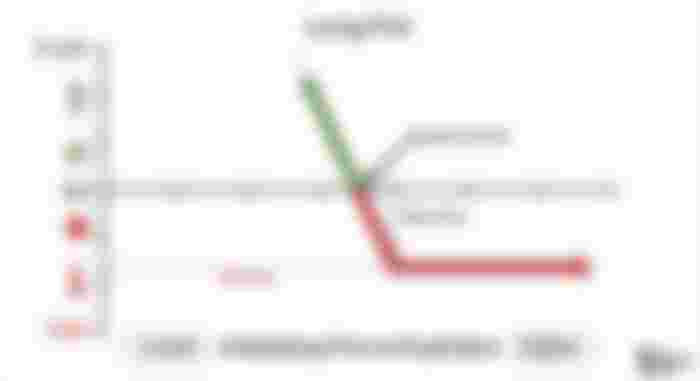

The seller has a concave position, because his gains are limited and losses are theoretically unlimited.

When it comes to the payoff curve and the unlimited loss, there are a few important differences in the crypto-sphere which we’ll cover later. For now, these are the payoff charts to keep in mind:

Belief the underlying will rise

Risk limited to premium paid

Unlimited maximum reward

Belief the underlying will fall

Risk limited to premium paid

Maximum reward limited to underlying reaching 0

Belief that underlying will fall

Maximum reward limited to premium received

Risk potentially unlimited (as the underlying price rises)

Can be combined with another position to limit the risk

Belief that underlying will rise

Risk “unlimited” to a maximum equating to the strike price less the premium received

Maximum reward limited to the premium received

Can be combined with another position to limit the risk

These profit and loss charts represent the simplest option trading strategy: buying or selling (long/short) just a single option, also know as single leg operations. When you combine them into multi-leg operations you can create complex strategies for different market situations, the possibilities here eclipse everything else for simple futures or altcoins trading.

Understanding these payoff curves is the most important thing for anyone interested in options trading, and we only have to cover those two convex operations.

Going long on Calls or Puts allows two important strategies:

1 – Use of massive leverage with limited downside.

2 – Safe hedge against a simple future position, which is much better than any stop limit order (those stops will be skipped on big market moves).

The same holds for crypto instead of stock

Options Moneyness & Pricing

Pricing of an options contract is influenced by four important forces:

Underlying asset price

Option strike price

Remaining time until expiration

Underlying asset price volatility

Underlying Price & Option Strike

To make the relation between options and the underlying easy to convey, they are classified into 3 categories:

ITM – In-the-money

ATM – At-the-money

OTM – Out-of-the-money

Suppose BTC price is currently at 24000USD: a Call with a strike price of 22000USD allows you to buy an asset worth 24000USD for just 22000USD. This option is said to be in the money.

A Call option at the money, in this example, would have the strike price at 24000USD or close by. And a Call out of the money would be above 24000USD.

Options in the money and at the money have another shade to differentiated them, this is common in most brokers or exchanges.

Put options are the exact reverse.

BTC at 24000USD, any option with a strike above 24000USD is in the money, because this contract means you could sell the asset for a higher price than what is currently worth in the market. Put options at the money will have a strike very close to 24k, and those out of the money have strikes below 24k.

Of course there is no free lunch, if you want to buy an option in the money you will pay more for the contract because they have intrinsic value, meaning, if the option were to expire at this very moment the contract would be worth something.

Conversely, the further you go out of the money, the cheaper those contracts get because they only have extrinsic value. Extrinsic value is like expectation value, maybe it will be worth something in the future, but right now there is nothing beyond the anticipation of possibilities.

The further out of the money is, the cheaper it gets.

Time

Time until expiration is another major force on the price of an option. All other variables being equal, expirations further away allow more “room” for the underlying to move into a profitable range, making them more expensive, as options get closer to expire they become cheaper. Ceteris paribus, OTM options lose value every day, like a dripping bucket.

But time decay is not linear, the closer it gets to expiration the more it accelerates, so you will find more options just a little OTM at the smallest price (currently 0.0005BTC) as they are about to expire.

Volatility

Volatility, like time, has a directly proportional result in both Calls and Puts. If the underlying’s price moves a lot, the chances of out of the money options getting in the money are higher, therefore all options get more expensive with higher vol.

There is a lot more about volatility, the misconceptions about market averages (Ludic fallacy), and the pricing indicators known as The Greeks, but we've got the basics covered so we’ll leave those topics for another time. Now we can get to those simple, yet powerful, strategies for beginners:

High leverage

Hedges

Simple Trading Strategies

High leverage can be like a siren call into to the “reking” rocks of liquidation. Some traders considered getting liquidated a badge of honor, or a rite of passage. This is but a rationalization for stupidity.

If you controlled your exposure as explained by part 1 getting a margin call won’t be as terrible as it is for most traders. Still, to avoid it, we’ll use subaccounts and the 3 types of leverage.

Just like the concept of moneyness makes the relation between underlying price and option clear, we can use a similar idea for risk and leverage.

As far as I know, Luis Fernando Roxo was the first to make this insightful distinction between the types of leverage. From terrible to good we have:

Toxic – When it goes wrong you end up owing more money than what you had allocated on your exchange.

Dirty – When it goes wrong you lose everything in your exchange.

Clean – When it goes wrong your loss is insignificant.

Currently in the crypto world toxic leverage is impossible. No exchange can take more than what you send to them.

In big exchanges from the old markets, toxic leverage is possible due to the intrusive kyc and regulation involved, if your trade goes completely south the exchange has a “legal” right to your property beyond what you have in your account. This can happen with naked option selling (the unlimited downside area of those Calls shorts).

This doesn’t make sense in the crypto sphere, but you never know with all the creeping regulations, so keep an eye for these possibilities in the future. Right now there is no need to worry about toxic leverage on any exchange, because the collateral remains in crypto. dirty leverage, however, is something to be aware.

If you ignore the steps we covered in part 1, you might be exposing yourself to dirty leverage. It can even be a matter of mindset, such as when you feel confident to the point of arrogance and increase your position size (on futures) or send more coins to increase your margin.

Premeditatio Malorum: The worst case scenario of 100% loss on the exchange has to be within your personal acceptable range before sending your crypto!

Keep your maximum losses small and under control. This is where the fractal barbel strategy comes into play, the base risks are covered which allow for bigger trades and returns with small amounts.

High Leverage

OTM options about to expire have an explosive nature, few traders believe in their potential, because (according to traditional models) the likelihood of those options expiring ITM is negligible. But those traditional models are based on false assumptions, although these options usually turn to dust, when they expire ITM, the payoff is so strong it makes sense to take small bets on them.

The explosive event of the Black Thursday (March 12) is the best recent example. Two days prior to the crash, Put options with a strike of 7000, expiring on March 13 were out of the money by at least 700 USD, and worth just 0.001BTC.

As the price plummeted, those options value exploded like few altcoins do, and each contract was worth 0.5BTC or more. Perfect example of antifragile convexity in action! While most traders were desperate during the fall, those who bought Put options had massive gains in BTC, to the point of compensating the drop and making a significant profit.

This strategy works best when volatility is low, which is not very common on BTC, and to make matters worse, those small constant losses aren’t easy for anyone’s mindset. Therefore, selecting or even adjusting the right amount of crypto you are willing to bleed before making a profit is tough and very personal. But worth the effort.

Upsides for OTM buying

Provides one of the largest payoff potential in crypto

Small upfront investment

Downsides for OTM buying

Requires patience and persistence

Only profitable with large and sudden price moves

Adjusting the amount can be difficult

The second simple option strategy is far easier, and if it doesn’t bring antifragility in the strict sense, it will bring resilience at the least.

Hedges

When trading regular futures, instead of relying on stops to control your losses, it’s much safer to make a hedge with options. Huge price moves can obliterate any stop trigger, on the other hand having an option hedge can bring peace of mind in those scenarios.

All you have to do is make sure your liquidation price is close to the strike of OTM options: Puts when your futures position is long, and Calls when short.

Let’s say you open a long position at 24000USD with a liquidation price at 19000USD. Set your stop at a comfortable range and buy Puts with a strike just above 19000USD in the same amount of your collateral size (1 contract is worth 1BTC, and can be divided by 10). Usually your stop will work, but if there is a big crash those Put will cover your loss. If your future position was a short just do the reverse and buy OTM Calls.

To minimize hedge costs, buy only options expiring within a week or less and way out of the money. Low costs also require that your liquidation price can’t be too close to your opening, but this is a good practice regardless. The longer you keep future position open, the longer you’ll have to roll this hedge forward, which will make a small dent on your profits.

To improve the risk exposure, you can combine this options insurance with subaccounts.

Deribit doesn’t have an isolated margin system, everything is under cross margin: the entire account’s balance is used as collateral. To isolated the margin there are subaccounts instead, this limits the maximum loss to the specific sub you are trading. It is an excellent system because it can be used to organize different trading strategies with no additional risk to your total exchange balance.

Upsides for Options Hedge

Covers the downside of a futures position with no risk of getting skipped like a stop order

Essential hedge (especially for long positions)

Downsides for Options Hedge

Has an extra upfront cost

Has to be managed as long as the position is open due to time limit

Remember I said there are a few important differences regarding the payoff curve and the unlimited loss in crypto?

Asymmetry of Bitcoin’s Payoff – Crypto Curve

When you account your profit/loss in USD, the above payoff curves images remain the same. Enthusiasts, however, care more about crypto and here is the catch.

Both collateral and payments are made in BTC.

The trading pair is BTC/USD.

Inside the platform the profit/loss is calculated in USD.

If you long BTC on the perpetual, as its value rises in USD, the crypto amount you get per extra dollar will diminish. Conversely, on the same long position, the crypto loss increases more as Bitcoin’s dollar value decreases.

Perpetual Long

Call Long (Blue), Call Short (Red)

This curved line is always present whenever there is a base currency (BTC or ETH) used for collateral and payments, combined with a quote currency (USD) for profit/loss calculation. We are using an asset for margin trading on the dollar price of that same asset.

The same curve would apply to for any combination of base/quote currencies, it’s nothing particular to crypto.

Due to this payoff asymmetry, a long position on futures requires more attention because the crypto loss is bigger when it goes wrong. Here lies the importance of sub-account control and Put hedges.

On the opposite trading, you gain more crypto with a short going well or a buying OTM Puts. Excellent news for net bears right?

Perpetual Short

Put Long (Blue), Put Short (Red)

Not quite, a bearish position has an extra risk with violent price drops. While they create exponential crypto gains for Futures short sellers and Put owners, on the other side of the trade, the pressure can cause too many liquidations for Futures long buyers and Put sellers. Which might deplete the insurance fund, leading to socialized losses.

Deribit (and other crypto derivatives exchanges) work as a bridge between traders. If too many traders get liquidated in a short time, there might not be enough coins to cover the winners. This is where the insurance fund comes in, it covers those trades up it’s maximum reserves. After that, the winners will simply have to accept a reduction in profits.

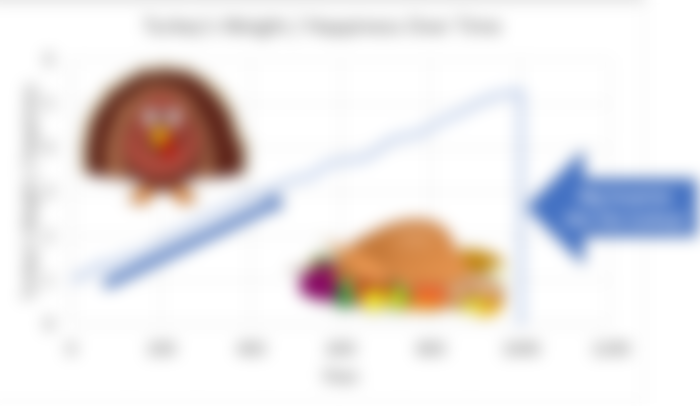

This almost happened during the Black Thursday event, sudden liquidations happening too fast took a tool. Had BTC price dropped lower, the insurance found would not have been enough to pay those Put owners and short sellers

Looks like the Turkey Problem doesn't?

They have improved their reserves for such events, but it’s another risk to keep in mind.

The key to convexity is control the downside, this is done before sending funds to an external private key. Insurance fund depletion is within the exchange risk we have already accounted for before starting to work on the upside, but it’s often forgotten or unknown by many traders.

Between the toxic leverage possibility on traditional exchanges and the socialized losses for crypto traders, I take the crypto world any time.

Antifragile Crypto Trading

Crypto brings more possibilities for individual liberty than any technology developed so far. It also exploded the traders barrier to entry like a cannon ball, now more opportunities for success are within reach for individuals throughout cyberspace. But with great liberty comes great responsibility.

Centralized exchanges play a crucial role in the ecosystem; although Dex’s are the ideal to be aimed, they are years away from technical maturity. It is hard enough to replace centralized spot exchanges, futures exchanges are far more challenging, especially on options.

While the barriers to entry made by fearful rulers still aren't insurmountable, my hope for this post is to add value and make experimentation on the crypto options world smooth.

Trade methodology is extremely personal, it will change between individuals, and even within each one throughout time as markets and personal knowledge change. Avoiding the risk of ruin, however, is an universal imperative.

May you achieve crypto financial independence!

Notes

[1] On Deribit all options are European: they cannot be exercised before the expiration date. However, it’s worth noting that they can still be traded prior to expiry (i.e. you do not have to hold it until expiry).

Exercising an option means putting the right specified in the contract into effect i.e. buying at the strike price of a call or selling at the strike price of a put.

Disclaimer

Instead of the old cliché this is not financial advice... here are the five rules of science from Neil deGrasse Tyson:

(1) Question authority. No idea is true just because someone says so, including me.

(2) Think for yourself. Question yourself. Don't believe anything just because you want to. Believing something doesn't make it so.

(3) Test ideas by the evidence gained from observation and experiment. If a favorite idea fails a well-designed test, it's wrong. Get over it.

(4) Follow the evidence wherever it leads. If you have no evidence, reserve judgment.

And perhaps the most important rule of all...

(5) Remember: you could be wrong. Even the best scientists have been wrong about some things. Newton, Einstein, and every other great scientist in history -- they all made mistakes. Of course they did. They were human.

Science is a way to keep from fooling ourselves, and each other.

Special thanks to:

Marco Batalha for the invaluable help with proofreading.

Thank you very much for reading!

If you like this article feel free to tip, share and subscribe.

Bitcoin - 1RenanWrFGvuPXefwF6Q2S7noqinQR54e

Bitcoin Cash - qzly3ntn6x7k7qw970vvlm8zlmzt2qnjxu6netzy8f

DAI - 0x6314526213b16aF52BBe227d06c1e8F1e662aa00

Dash - XoCRnBqGFMjdP8PwKfF7Rrb8hnCKLbE27A

Decred - DsacQEaY9gXT6Bjvx9U1SLH3YbhHhkLBhjE

Ethereum - 0x6314526213b16aF52BBe227d06c1e8F1e662aa00

Monero - 4418L4CxTQsa6hz26bEtfEBW4iFvnRfYw6A6gq1Up6qQFLsR8NS5qyvKXc1HieV4HFP2vPF84YwEw9QWDWrnk2uRBA2yqFq

Nano - nano_1r15f1naypwn87zxq75ztx7pdx3ao9hspehh1jijjhb9c3a5jn6kc7ske9gn

NEM - ND6OZRXOWIXHTAOW4YBWDNXKGHLQWYVSU4WGGVPL

Zcash - t1fkoBKABLETDcNQg9XXxhh3ikswvhPf899

Contact - Keybase