Are you brand new to crypto and not sure where to begin to learn about it? Check out my intro to cryptocurrency and intro to blockchain posts or my cryptocurrency blog to learn more about this fascinating new technology!

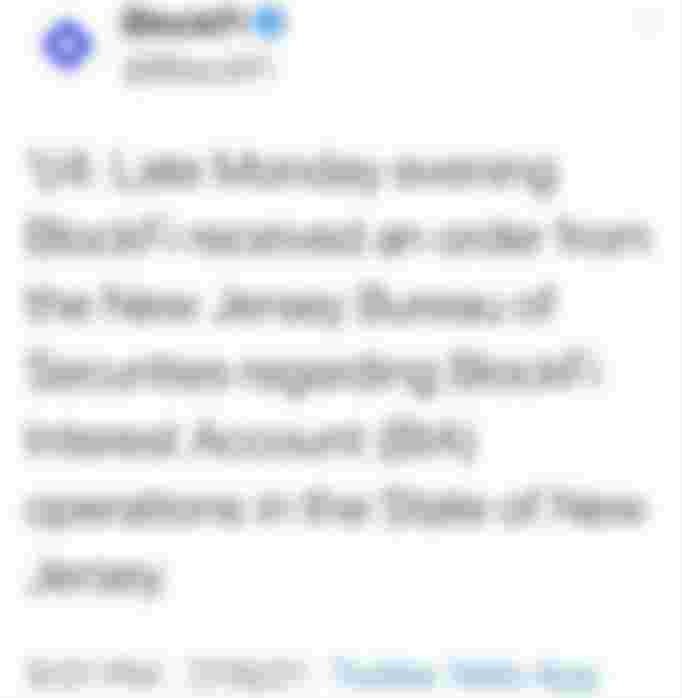

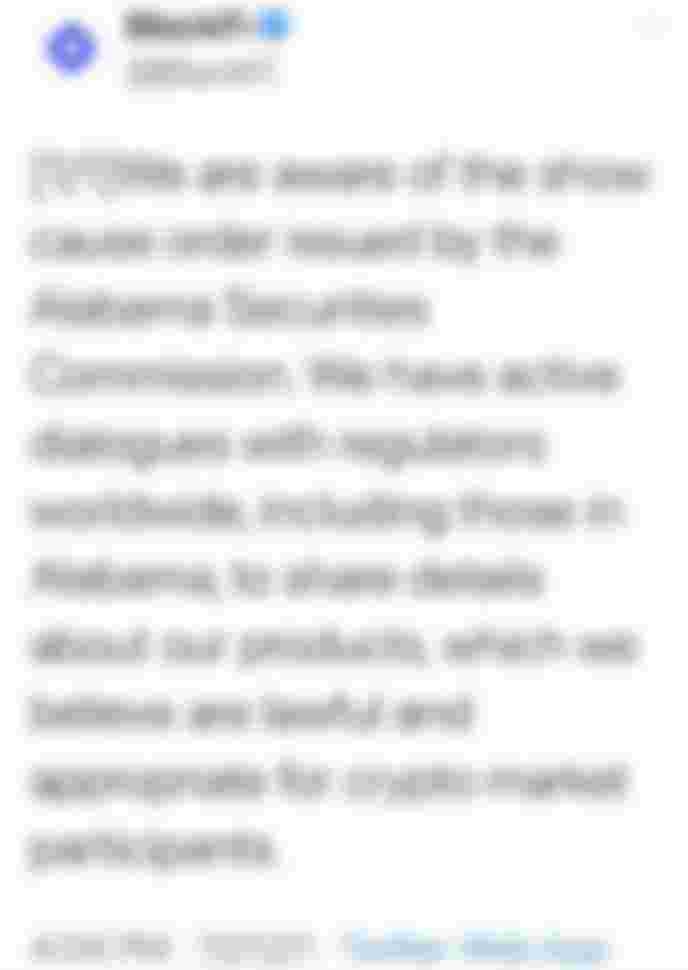

It has been said that all publicity is good publicity. But when it comes to actions by regulators against cryptocurrency and the companies that operate within the space, that is, more often than not, a false statement. BlockFi is the latest crypto entity to be on the receiving end of a government's wrath, having received not one, but two different regulator inquiries in the last several days:

These actions by the states of New Jersey and Alabama demonstrate that the governments of the world have no intention to stop flexing their regulatory power against cryptocurrency, blockchain, and everything in between. There are likely a variety of reasons why governments rail against cryptocurrency. Regardless of the reason, their behavior should come as no surprise to seasoned participants in the space. After all, from its earliest days, the main ethos of many cryptocurrencies has been separation from control by any one government, company, or person.

In the short-term, these developments will be detrimental to BlockFi’s prospects. And they have already been detrimental to cryptocurrency markets in general as prices collectively shed an average of around 10% in the 36 hours after the initial announcement. However, there are many reasons to believe that, over the long-term, crypto financial services specifically and cryptocurrency in general will continue to flourish. Before we get into that though, let’s get a bit more background on BlockFi and what may have driven its recent regulatory woes.

BlockFi: Banking the Crypto World

BlockFi participates in the ever-expanding world of crypto-banking and crypto financial services. The industry is rapidly becoming crowded, and BlockFi competes with a host of similar companies like Celsius Network, Nexo, Abra, and others. However, BlockFi states the following regarding the differences that set it apart from its competitors:

BlockFi sets itself apart from other cryptoasset service providers by pairing market-leading rates with institutional-quality benefits.

A rather generic statement all in all from the company. However, as a user of both BlockFi’s services and those of several of its competitors, I can share my own opinion and say that BlockFi does have a slightly more institutional approach to its product offerings than its competitors. I’ll let you be the judge as to whether or not that is a good thing.

BlockFi provides a variety of services to its customers. Retail users are able to exchange fiat, stablecoins, and cryptocurrencies from one to the other, receive crypto-collateralized loans, use the company’s Bitcoin rewards credit card, and more. Institutional users on the other hand are able to borrow assets deposited with BlockFi for use in a variety of investment strategies. However, it is the company’s flagship product, the BlockFi Interest Account (BIA), that ruffled regulator’s feathers this week.

The BIA is actually rather simple. Open an account, deposit your cryptocurrency into BlockFi’s cryptocurrency wallet, and receive interest from the company on your deposits once per month. If the business model sounds familiar, it should. The product is a traditional savings account through and through. There are, of course, two main differences: the accounts are almost always denominated in cryptocurrency and stablecoin rather than fiat, and the accounts typically pay interest rates of ~4-12% that seem massive when compared to the paltry fractions of a percent offered by most traditional savings accounts these days.

In a nutshell, securities regulators in both New Jersey and Alabama have expressed concern that BlockFi’s Interest Accounts may be partially funded by unregistered securities or may be unregistered securities themselves. Without seeing the actual documentation from the regulators, it’s hard to know what is driving their concerns. However, we can make an educated guess.

Regulators worldwide are all over the map when it comes to labeling cryptocurrencies. Are they property, currency, securities, or something else entirely? The U.S. Securities and Exchange Commission (SEC) has previously said that it believes Bitcoin and Ethereum do not currently operate in a way that makes them securities. After all, neither cryptocurrency is controlled by a company nor can either be closely associated with any company. That is not necessarily the case for several other cryptocurrencies that BlockFi accepts on its platform:

Uniswap

Uniswap is the governance token of its namesake DeFi protocol. As such, it is used by holders to vote on how the protocol should run and on any changes that should be made. A governance token, even for a decentralized platform, functions very similarly to a corporate stock. As we know, corporate stocks are defined as a type of security in most parts of the world. Could New Jersey’s and Alabama’s regulators be insinuating that they think Uniswap is a security too?

Basic Attention Token

The Basic Attention Token (BAT) could perhaps be called a rewards token based on its functionality. Users of the Brave internet browser receive BAT in exchange for their attention to ads that run on the platform. The token itself is managed quite closely by the Brave company. The token doesn’t represent ownership in the company, nor does it give holders any ability to govern the company. However, regulators have commonly parroted comments from critics asserting that cryptocurrencies have no value or backing. Could regulators have gotten the impression that BAT represents some sort of liability on the balance sheet that the Brave company is selling to its users?

Defiance through DeFi

Regulators and governments have always come after companies that they disagree with and they will continue to do so well into the future. After all, there’s little stopping them. They make the law and the companies either reside within their borders or are trying to sell to customers within their borders. And it’s so easy to go after a centralized company. Just Google their address and send the cease and desist letter right over.

For these and other reasons, we are highly likely to see centralized crypto companies begin to shrink and DeFi platforms continue to grow over the coming years. DeFi platforms are much harder for governments to regulate because there typically isn’t a public entity to go after. There may be a developer team, but tracking them down over Google would almost assuredly be impossible. Even if governments did manage to take the developers offline, those developers commonly have just a small amount of control over the system, meaning that most of the DeFi platforms would continue to operate relatively smoothly.

While centralized companies will argue that they have a place in the crypto-world, they will always stand on rocky footing. They will continuously be subject to the whims of governments and regulators the world over. And that puts them at a significant disadvantage against decentralized platforms that are relatively immune to government oversight. In the past, companies that were able to operate more freely and give consumers what they want have, by and large, been more successful than peers that could not. Why should DeFi versus CeFi be any different?

If you found the above post to be helpful, please consider supporting me by providing a small tip below.

Interested in learning more about Bitcoin, Blockchain, and Cryptocurrencies?

The following links are for companies that I personally use and recommend. You are under no obligation to sign up for their services or review their content. However, I may receive some small form of compensation if you do click the links and sign up and that compensation helps support me in my efforts to educate people about cryptocurrency and blockchain:

BlockFi provides cryptocurrency exchange and custody services, interest-bearing cryptocurrency accounts, and more! Open a new account and earn $10 in free Bitcoin when you deposit your first $100 on BlockFi.

Coinbase provides cryptocurrency exchange and custody services, cryptocurrency staking on several blockchains, and more! Open a new account and earn $10 in free Bitcoin when you buy or sell your first $100 on Coinbase.

Nexo provides interest-bearing cryptocurrency accounts, crypto-collateralized loans, and more! Open a new account and earn $10 in free Bitcoin when you deposit your first $100 on Nexo.

Publish0x allows you to earn crypto for reading crypto news and interacting with crypto bloggers, 100% free of charge.

Well, I think DEFI platforms are coming into regulatory oversight too... they are becoming institutional - KYC disclosure etc. Aave has one KYC needing platform for institutions.

There is definitely going to be a tussle between Govt. and DEFI platforms, as their CEO's are known in some platforms and that's enough to harass them with regulatory stuff.

Anyway... I withdrew my crypto from Celsius coz its centralized, although it did give interest rates for depositing cryptos in cryptos and its CEL token is doing well.

Somewhere, we feel better to have control of your funds than give control to 3 rd parties as you be in space for a while.