Hi everyone!

With these unprecedented days, overly expenditure could easily happen, while your wages might not be as much as you liked.

This particularly easily happen when you have a car, mortgage and family needs. All these can suddenly happen, and you can choose whether these Emergency funds should be invested in crypto or not, and how easily you can withdraw when things happens.

Today is the final day of January, and if you have been diligently tracking your expenses, you should be able to chart something out simply with a chart to know where is permanent expenses, and which one can be cut down.

For me, every January and Jun I will have a whopping 48.6% expenses all to housing, which totally have no more savings (in fiat) because of the half yearly payments and also monthly mortgage.

These are unavoidable expenses, and of you have the heart to own a place of your own, if you have anything excess at the moment, take the opportunity to see if you can set aside at least 30% of your income aside for the future expenses for your home.

If you don't have that extracted from your usual income, this means you should start planning if there is a way find other means like investment in compounding crypto that you know is still increasing in value to grow your savings, or take the opportunity like earnings here in payable blockchain blogs to help you grow that future home of your own.

What if I just want to use my fiat to work for me?

It is still possible...

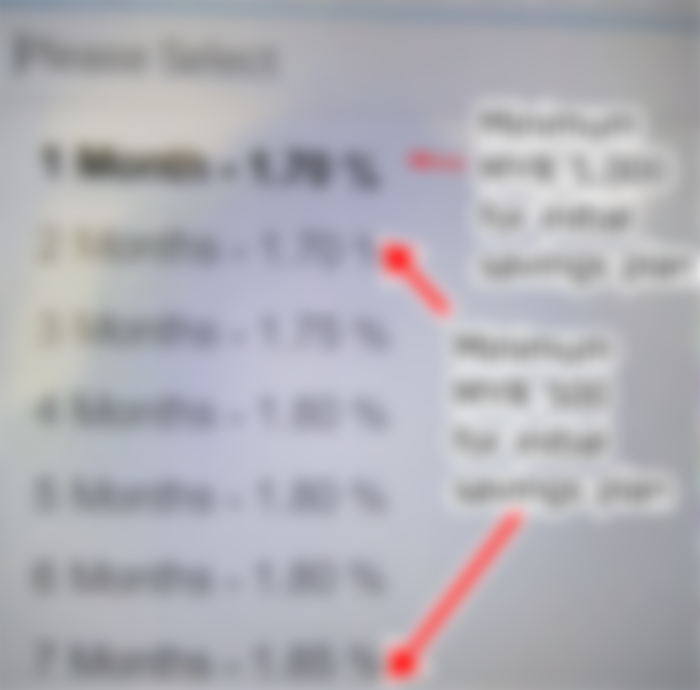

Even very unfortunate like in Malaysia, it requires at least 10,000 MYR to earn a 2% per annum dividend (which is very saddening, I know - because it used to be 6%), there are bank packages you can still look into should you require almost immediate liquidity.

For example some banks still offers minimum tenure lockup for savings, however if you have even less than that, probably you might need to look into dollar cost average savings into crypto, but you must be very certain those funds invested into crypto would probably have to stay in your wallet / centralised compounding services like Celsius or Nexo for a while if you want to profit on the long run.

Therefore, if you want to have something big, like a home, always plan your savings at least 2 years ahead.

Better still, if your first salary has already start saving aside, because you have yet to have any liabilities and obligations in life.

But there is one crucial thing:

Never ever place all your savings under one portfolio - crypto. If you have bank services that is still a tiny bit profitable, you should consider 20% crypto - 80% fiat at the moment and slowly work your way up in your savings portfolio because at this day and age, the world system still use fiat currency, but if the worse has started, then you probably need to diversify yourself in different crypto and even precious metals (even though it is not as popular anymore) unless you are very confident with stock market trading.

So far, the compounding services Nexo (for example) its token is still increasing despite of volatility values compared to choosing stable coins to compound upon, so this is something you can think and consider, when you choose to place your savings into a (possible) volatile digital or a stable digital asset, and because of the uncertainties, constant observations (like a weekly basis) is important to check if your savings are going down the drain or accumulating better value.

That being said, always remember that centralised compounding services will not guarantee you investment safety. It is never " #SAFU " (Secure Asset Fund for Users) despite the services would assure to you; because:

If you are not holding your private keys, those crypto doesn't belong to you as it is loan out for the service to generate income for you.

It is the same with Fixed Deposit in Banks, although in Malaysia there is actually insured services for these benefits, but it is a must to double check to be sure.

Well, I hope that this gives you some idea how you can plan ahead and how to structure your savings from your regular income.

How's your country's financial and banking situations?

(if you are not from Malaysia?)

How do you cultivate your saving aside habit, or you have never start yet?

Would love to hear from your side of the story.