Latest CBDC Report - You Have to Read It!

The adoption of crypto has produced a lot of pressure on governments around the world. Now, they are trying everything in their power to design their own central digital currency before they lose their power. In this article we will take a look at a recent report that outlines some plans for CBDC. Keep in mind that this article is not financial advice but only for entertainment purposes. With this being said, let’s look at the propositions this article is making and how this is one of the dumbest articles you will ever read. Background of the Report Before we deep into the report a few background information. The report was made by the BIS (Bank of International Settlements). This can be described as the bank for Central Banks and has several members like the European or the United States Central Bank. Over the last few years, the SIC was trying to make a plan for Central Bank Digital currencies (CBDCs). A little disclaimer in this regard. CBDCs should not be regarded as a cryptocurrency! The obvious reason why are as follows. CBDC are centralized, offer no privacy and are permissioned. In other words: it is everything what I as a crypto fanatic don’t want in the first place (with some exceptions of course). The report we will be talking about is describing how this CBDC should look like and is divided into the following parts (also linked in the sources): · Design and Interoperability · User Needs and Adoption · Financial Stability Implications CBDC Design One of the most important information that this report covers is that this CBDC will be used by the retail and private sector. This implies that the people in power will be using a complete different CBDC as us normal people. This should be the first red flag.

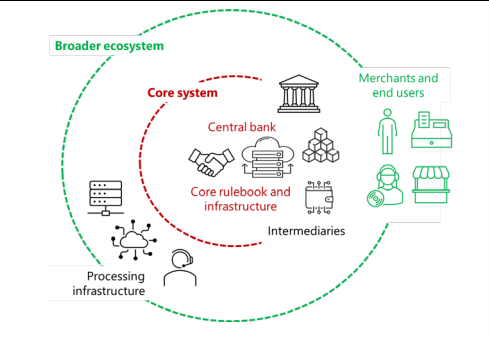

Continuing with this report, the CBDC is supposed to be issued and being controlled only by the central entities which are in power. While the Central Banks want even more control over all of the transactions, they are not planning to cut out service providers like Visa just because they haven’t got the infrastructure. The following picture should help to illustrate how the future ecosystem with a CBDC is supposed to look like:

Given that private institutions are supposed to be a part of this ecosystem means that CBDCs have to be interoperable not only internationally but also domestic. This would lead to a lot of technical issues and that’s why the report suggest limiting the amount of the private intermediaries who are then selected by the Central Banks. Red Flag number two and if you ask me a big attack on the liberty of the free market. With this being said let’s jump onto the next red flag that is waiting right around the corner to stab us in the back. According to this report “full anonymity is not plausible”. Thankfully the provided data would be safe with the explanation that the Central banks would have no commercial use for this kind of data. Furthermore, every transaction amount above a certain threshold will be tracked. Adoption Plans and Potential Effects This brings us to the next part of this report which explains how the Central Banks plans to adopt their CBDCs. The context of this adoption would be very hilarious. The main reason why the Central Banks are doing all of this is because of the mass adoption of cryptocurrencies and they are worried that users may adopt “other, less safe instruments, potentially leading to economic and consumer harm”. Right! In my opinion somebody is afraid to land on the substitute bench. Reading further, this report admits that due to technological advancement payment methods are getting cheaper, safer, and faster. But instead of letting these innovations to continue the BIS thinks it is better done in a completely different way. The report then goes to show how this CBDC adoption could be achieved. The points are: · Fulfilling User Needs · Achieving Network Effects · Keeping the Usage Device of the User With these in mind, the main arguments that the CBDS has are security, high liquidity, low costs, and privacy. So, everything that we already getting with cryptocurrencies? I lost count with the red flags, but this seems like the twentieth one! As the report goes on the main adoption techniques are revealed. It looks like the BIS is planning to “incentivize consumer use of CDBC by disturbing social benefits and transfers to individuals in CDBC”. Pretty manipulative if you ask me. Financial Stability Implications This brings us to the third part of this report, and this is the financial stability implications and its effects on the economy. One of their main arguments towards a CBDC is that Stablecoins are not that long in development and need to satisfy the regulators. The truth cannot be further away: Stablecoins are already around for years, and users slowly know which Stablecoins to trust and which not. Additionally, the report claims that Stablecoin issuers are not designing their product to be interoperable with other forms of money. By this point you should be rolling on the floor and laughing your tears out but if you are still here the report continues. The report shows a little bit of its real intention with the following quote: “Significant Stablecoin adoption and […] could result in excessive market power and […] described as a risk for CBDC issuance”. This statement confirms that Stablecoins are being seen as a big risk and my guess is that this is the reason why so many regulations are on their way. The next part of this report describes the risks that the CBDC could implement on the banks. In times of crisis the CBDC could be seen as a good investment. This would mean that people would move their money out of the banking system and into CBDC. Inevitably, this leads to a collapse of the banking system. Even without the crisis there would be a big risk on maintaining the private bank sector. This is why the report suggests some measures to maintain it. Some of these are: · Reduction in assets/ deleveraging · Increased lending rates · Switching to alternative market-based funding sources which could be more expensive and, in some cases, less stable These suggestions would lead to unaffordable loans or even the forbidding on taking loans which seems very laughable to me. But at this point of this report everything seems to be possible. Even the forbidding of buying CBDC during time of crisis seems to be possible. Conclusion In my opinion this report shows one thing. It will be very difficult to roll out and adopt such a project. Not only do people right now have better alternatives like crypto, they also feel more freedom with these. With the adoption of such a CBDC I only see the power shifting to banks even further and this has to be prevented at some point if this world should not be ruled by corrupt institutions. To calm all of you down I have to add that CBDC is long time from happening and that only time will tell if this could be successful. In the mean time I am very curious how the crypto space will develop and what new amazing projects are around the corner! Published by ga38jem on Publish0x|LeoFinance|Steemit|read.cash On 15th October 2021 Sources: https://www.bis.org/publ/othp42_system_design.pdf https://www.bis.org/publ/othp42_user_needs.pdf https://www.bis.org/publ/othp42_fin_stab.pdf https://www.bis.org/publ/othp42.pdf

No comments yet