My understanding of how DEFI lending business using crypto as collateral works for AAVE protocol

From AAVE protocol's website https://aave.com/ Wondered how lending DEFI businesses run sustainability using crypto as collateral Initially, few years back I would have been afraid to invest in cryptos, as I would not be able to adjust to its volatility but over the years I have learned to cope with its price ups and downs, because it’s actually exciting and not that risky if you learn to invest more smartly. However, I could not understand how the lending and borrowing side of business in DEFI using crypto works, because of the price volatility of the crypto collateral used for these purposes. Cryptos are subject to a fluctuating value and are more volatile than traditional collateral like real estate used for taking loans. The price of the underlying crypto asset has to cover the costs of the loan liabilities incase of default in payments.

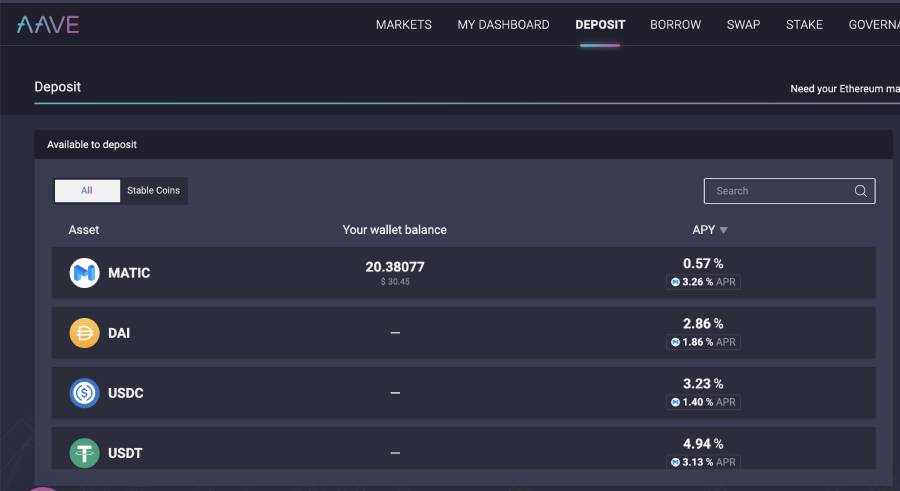

I am now understanding how DEFI borrowing and lending operations function sustainably even though these protocols use crypto collaterals for these purposes. Ventured to check out the lending DEFI protocol AAVE in Polygon I started dabbling with DEFI ever since I got into the Polygon ecosystem, which is an alternate network to check out some well established Ethereum DEFI apps in a cost effective and convenient way. https://read.cash/@bulletgelly/a-crypto-enthusiasts-first-proper-defi-experience-using-the-polygon-network-c244263d One of the first DEFI apps I tried out was AAVE which is a very popular non-custodial DEFI borrowing and lending platform known to be secure to use as its a well established audited protocol. Understanding the way AAVE protocol works I started off by depositing my Matic and Ethereum cryptos to earn interest. These deposits earn interest because they are assets which are lent to borrowers.

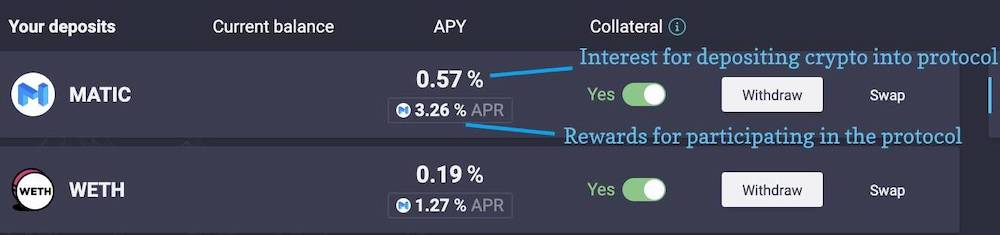

After doing this, I took my time to understand AAVE to figure out how the protocol functions by reading the faq and risk parameter details given in AAVE document links here - https://docs.aave.com/faq/borrowing and here https://docs.aave.com/risk/asset-risk/risk-parameters . Earning interest as a LP provider by lending cryptos in the AAVE protocol Then I understood that by depositing my cryptos for lending in the protocol I have become a Liquidity Provider(LP) for AAVE and I earn interest and rewards in Matic tokens. I earn interest for the amount given for lending and I get rewards for participating in the AAVE protocol.

Borrowing against deposited crypto collateral to earn more Matic tokens After this I ventured further more by borrowing against my lent cryptos and this is where I got some understanding of how these protocols function sustainably using crypto collateral. As a borrower it’s true I have to pay back the loan amount with interest but I also get rewarded again in Matic for participating in the AAVE protocol in Polygon Blockchain. Here I earn more Matic by borrowing against my deposits.

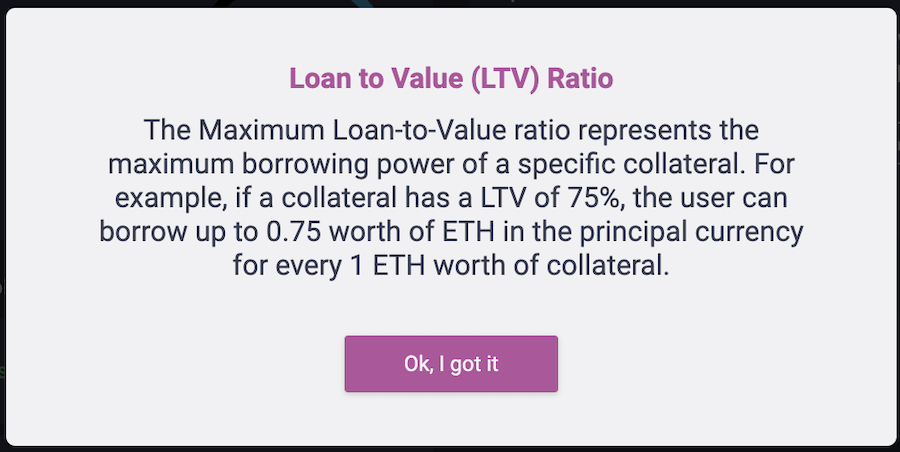

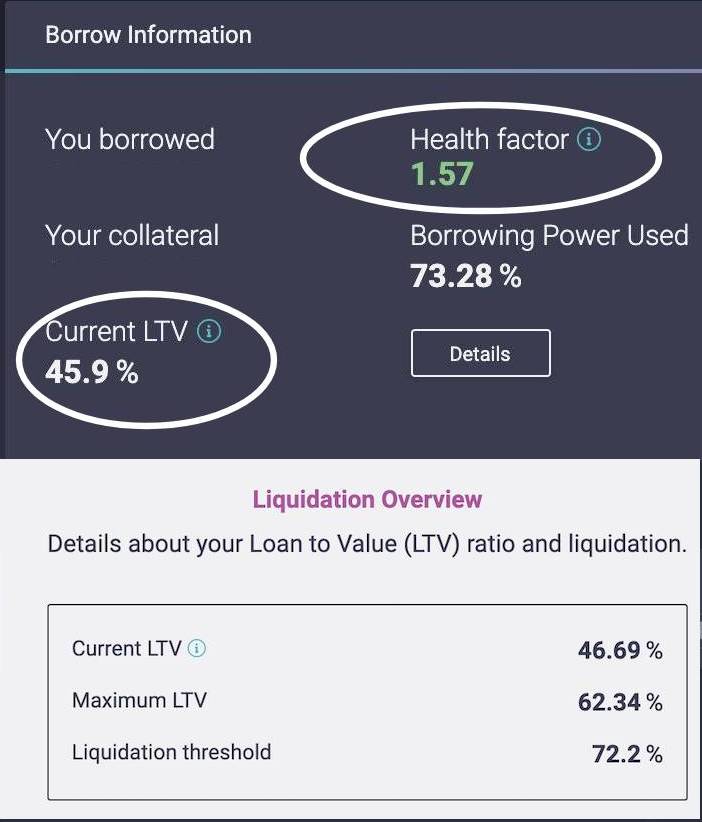

*Borrower needs to pay interest on the loan borrowed, but earns Matic rewards for participating in the protocol* I borrowed Matic crypto which I again deposited to earn more interest. I am able to understand that people borrow more crypto to earn more interest in ways like this. The idea is simple that one earns enough Matic through interest earned by lending and through protocol participation rewards that will easily compensate for the interest one has to pay back when repaying the loan amount borrowed. Understanding the risk parameters of these DEFI protocols to prevent liquidation of collateral However, one has to be aware of certain crucial aspects of the way the DEFI protocol functions, when venturing to do these borrowing activities so that the deposits we have provided as collateral don’t stand to get liquidated. ***This is why when participating in any DEFI protocol we must understand the risk parameters involved.*** The risk parameters to understand here are the Loan to Value (LTV) ratio, Liquidity Threshold, Health Factor(HF) and more such parameters whose explanation is given in the document links I provided earlier. Borrowing amounts are fixed and limited by the LTV ratio Since the underlying value of the crypto collateral is subject to fluctuation according to market conditions, it is made possible for the borrower to only borrow amounts that are a certain percentage of the collateral value.

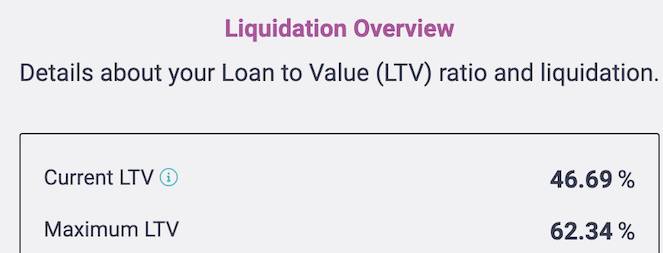

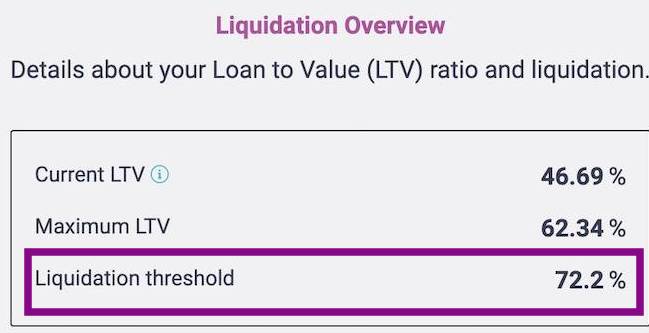

*Loan to Value Risk Parameter* For example, in my case for the Matic and Ethereum cryptos I have given as collateral, I can borrow only 62% of my collateral value. However I have taken a loan amount that is equal to only 46% of my current collateral value.

This is LTV ratio, where one is allowed to take loans that are only a percentage portion of the crypto collateral provided. This ensures that the loan value taken is lesser than the value of crypto collateral so generally loans taken against crypto collateral are over collateralized making allowance for the possibility of the crypto value to fluctuate downwards. This practice is followed to ensure that the value of the loan taken is always covered by the value of crypto collateral provided. Liquidation of Collateral if its value falls below what’s permitted in the Liquidity Threshold parameter AAVE protocol has rules on when your crypto collateral is subject to get liquidated which is defined in the risk parameter known as Liquidity Threshold. In my case if the value of my loan goes to 72% of the crypto collateral I have provided then my loan will be considered under colaterised and is subject to get liquidated.

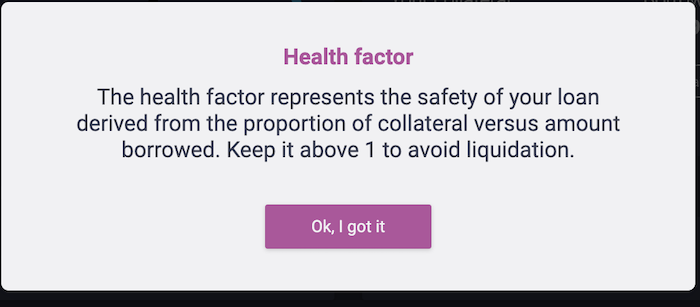

Liquidity threshold defines the maximum limit to which the loan value can rise against the given collateral, as a rise beyond that percentage limit will trigger liquidation of the collateral provided. There are liquidators that are incentivised to liquidate collateral that have crossed the Liquidity Threshold limit. Keeping track of the Health Factor value to know the safety status of the collateral against liquidation A very important parameter for borrowers to keep an eye on is the ***Health Factor (HF)***. The Health Factor denotes how safe your crypto collateral is against the risk of liquidation. ***The thumb rule is to maintain a Health Factor value >1, as when the HF value reaches 1, one’s collateral is subject to liquidation.***

The HF value will fluctuate according to the fluctuation of the value of the collateral provided against the loan value. Therefore, when the value of the crypto collateral provided appreciates against the loan value , there will be an increase in HF factor and when the value of the crypto collateral declines against the value of the loan, the value of the HF factor reduces. The value of the HF sets according to the changes and variations that happen with the Liquidity threshold. Monitor the risk parameter values on a daily basis to ensure one’s collateral is not at the risk of getting liquidated All these parameter values will be available for users to monitor in the dashboard of AAVE platform. It’s a good practice for borrowers to monitor their Health Factor values and take steps to ensure that their collateral status is safe against the possibility of liquidation.

*Risk parameter data should be monitored on a regular basis from the dashboard* One can either repay back the loan with interest(that should not be an issue as interest for lending and for protocol participation would be accrued), or add more collateral to bring the value of the collateral to maintain safe LTV and Liquidity threshold levels. Monitor the price of cryptos and hold crypto collateral accordingly

*Matic price chart taken from* *trading view* https://www.tradingview.com/chart/jCWaxKNy/ *Safer to borrow with crypto collateral when crypto prices are experiencing an upside momentum, and not borrow with crypto collateral when prices are going to decline to the downside.* For the past month, the value of my cryptos(Ethereum and Matic) that I have deposited as collateral has been increasing so I considered it safe to borrow against my collateral at a time when crypto prices are experiencing price rises being in a bull run. I am keeping an eye on crypto prices, their next major resistance levels where the crypto prices will be subject to a price correction phase etc, based on which I will close my loan position while I earn some additional Matic for all these DEFI activities. This is all I understood from my DEFI lending and borrowing experience from AAVE. AAVE has made provisions to maintain protocol Solvency AAVE maintains ecosystem reserves, where a portion of the interests the protocol generates is kept in a collector contract. This is called reserve factor and all the rewards protocol participants get come from this ecosystem reserve. AAVE’s reserve factor provision is a safety module made to maintain the protocol’s solvency. The cost of providing additional incentives by the protocol will be covered by the reserve factor. ***Thank you for reading my post. Good day!!***

No comments yet