Final part of the article on everything you need to know about cryptocurrency trading:

Researchers will also focus on comparing classic statistical models and machine/deep learning models. Rane et al. described classic time series forecasting methods and machine learning algorithms used to predict bitcoin prices. Comparing statistical models such as Autoregressive Integrated Moving Average Model (ARIMA), Binomial Generalized Linear Model and GARCH with machine learning models such as Support Vector Machine (SVM), LSTM, and Nonlinear Autoregressive Exogenous Input Model (NARX) . Observation results show that the prediction accuracy of NARX model is close to 52% at 10 second intervals, which is the best prediction model. Rebane et al. compared the difference between traditional models such as ARIMA and modern popular models such as seq2seq in predicting cryptocurrency returns. The results show that the seq2seq model is significantly better than the ARIMA model in terms of bitcoin dollar forecasting, but in extreme cases, the seq2seq model shows very poor performance. The author recommends additional investigations, such as using LSTM instead of GRU units to improve performance. Stuerner et al. also compared similar models. They discussed the advantages of automated investment methods in cryptocurrency trading trend tracking and technical analysis. Samuel et al. explored a vector autoregressive model (VAR model), a more complex RNN, and a mixture of the two in the residual recurrent neural network (R2N2) for predicting cryptocurrency returns. The RNN with ten hidden layers is optimized for the settings, and the VAR-enhanced neural network makes the network shallower and faster than RNN, and has better predictive capabilities. Compare RNN, VAR and R2N2 models. The results show that the VAR model has a significant test period performance, which supports the R2N2 model, while the RNN model performs poorly. This research aims to optimize the model design and apply it to cryptocurrency revenue forecasting.

Sentiment analysis

Sentiment analysis is a hot research topic in the age of social media, and it is also used to improve the prediction of cryptocurrency transactions. This data source usually must be combined with machine learning to generate trading signals.

Lamon et al. used daily news and social media data to label actual price changes instead of positive and negative sentiments. In this way, price predictions are replaced by positive and negative sentiments. The experiment obtained headlines of news articles related to cryptocurrency from websites such as "cryptocoinsnews" and twitterapi. In the cryptocurrency market, weights are represented by positive and negative numbers. Comparing Logistic Regression (LR), Linear Support Vector Machine (LSVM) and NB as classifiers, it is concluded that LR is the best classifier for daily price prediction, with a correct rate of 43.9% for price increases and a prediction for price drops The correct rate is 61.9%. Smuts used the LSTM model using Google Trends and Telegram sentiment to carry out a similar price prediction method based on binary sentiment. Specifically, this sentiment was extracted from Telegram using a new method called VADER. In the first half of 2018, in terms of predicting hourly prices, the accuracy of back-testing on the test set reached 76%. Nasir et al. studied the relationship between cryptocurrency revenue and search engines. The experiment uses a rich set of empirical methods, including VAR framework, copulas method and non-parametric time series graphs. It turns out that Google search has a significant impact on Bitcoin yields, especially in the short term. Kristoufek discussed the positive and negative feedback on Google Trends or Wikipedia's daily views. The author proposes different methods to find the causal relationship between prices and search terms in the cryptocurrency market, including cointegration, vector autoregression and vector error correction models. The results show that search trends and cryptocurrency prices are related. In the experiment, there is also a clear asymmetry between the effects of increasing interest in currencies above or below its trend value. Young et al. analyzed user comments and replies in online communities and their relationship with cryptocurrency volatility. After collecting comments and replies in the online community, the authors marked the range of positive and negative topics. Then, test the relationship between the price of cryptocurrency and the number of transactions based on the comments and responses to the selected data. Finally, based on the selected data, a prediction model based on machine learning was established to predict the volatility of the cryptocurrency market. The results show that the amount of data accumulation and active community activities have a direct impact on the price and quantity of cryptocurrencies.

Similarly, Colianni et al., Garcia et al., Zamuda et al. and others applied sentiment analysis techniques to the field of cryptocurrency transactions, with similar results. Colianni et al. cleaned up data and applied supervised machine learning algorithms such as logistic regression, naive Bayes, and support vector machines in Twitter sentiment analysis of cryptocurrency trading. Garcia et al. applied multi-dimensional analysis and impulse analysis to the social signals of Bitcoin sentiment effects and algorithmic trading. The research results validated the long-term hypothesis that transaction-based social media sentiment may generate positive investment returns. Zamuda et al. adopted a new sentiment analysis indicator and used multi-target portfolio selection to avoid risks in cryptocurrency trading. Based on the elastic demand of cloud infrastructure for computing resources, this view is rationalized. A general model for evaluating user network behavior-response-impact model (ARIM) is proposed. Bartolucci et al. used the "butterfly effect" to study the price of cryptocurrencies, which means that the "problems" of open source projects provide insights to improve cryptocurrency price predictions. The sentiment, courtesy, and sentiment analysis of GitHub comments is applied in the Ethereum and Bitcoin markets. The results show that these indicators have predictive power for cryptocurrency prices.

Reinforcement learning

The in-depth enhancement algorithm bypasses the forecast and directly enters the market management action to achieve high cumulative profits. Bu et al. proposed a combination of dual-Q network and unsupervised pre-training, using DBM to generate and enhance the optimal Q function in cryptocurrency transactions. The transaction model contains two serial agents in the form of neural networks, an unsupervised learning module and an environment. Enter the market state to connect to the coding network, which includes spectral feature extraction (convolution pool module) and temporal feature extraction (LSTM module). The double-Q network follows the coding network and generates actions from this network. Compared with the existing deep learning models (LSTM, CNN, MLP, etc.), this model achieved the highest profit even under extreme market conditions (24% profit was recorded, while the cryptocurrency market price dropped -64 %). Juchli applied two implementations of reinforcement learning agents, one is Q-learning agents, which act as learners without market variables, and the other is DQN agents, which are used to process the aforementioned features. The DQN agent was back-tested under two different neural network structures. The results show that the DQN-CNN agent (convolutional neural network) is superior to the DQN-MLP agent (multilayer perceptron) in terms of backtracking prediction. Lucarelli et al. focused on improving automated cryptocurrency transactions through deep reinforcement learning methods. A comparison of the double deep Q learning network and the double deep Q learning network was carried out for 4 years. By setting the reward function as the Sharpe ratio and profit, it is proved that the double-Q learning method is the most profitable method in cryptocurrency trading.

Other

Atsalakis et al. proposed a computational intelligence technology that uses a hybrid neuro-fuzzy controller PATSOS to predict the direction of changes in the daily price of Bitcoin. This method is superior to the other two computational intelligence models. The first is developed with a simple neuro-fuzzy method, and the second is developed with an artificial neural network. According to the signal of the model, the investment income obtained through trading simulation is 71.21% higher than the investment income obtained through a simple buy and hold strategy. This is the first application proposed in Bitcoin price change prediction. Literature applies topological data analysis to price trend prediction in the cryptocurrency market. This method uses the topological characteristics of the attractor of the dynamic system to process data at any time. The results show that this method can effectively separate important topological patterns and sample noises (such as buying and selling rebound, discreteness of price changes, difference in transaction size or information content of price changes, etc.) and provide theoretical results. Kurbucz designed a complex method consisting of a single hidden layer feedforward neural network (SLFN) to:

(i) determine the most frequent edge of the transaction network (a public ledger that records all Bitcoin transactions) against the future price of Bitcoin And

(ii) provide an effective technique to apply this undeveloped data set in day trading.

The study found that based on the information available from a small number of edges (about 0.45% of all unique edges), the accuracy of price change classification is very high (60.05%). It is worth noting that Kondor et al. first published some papers to analyze the trading network in the cryptocurrency market, and conducted related applied research on identifying Bitcoin users . Abay et al. tried to use topological features to understand the network dynamics behind the blockchain graph. The results show that standard graph features such as the degree distribution of the transaction graph may not be sufficient to capture network dynamics and its potential impact on Bitcoin price fluctuations. Maurice et al. applied wavelet time scale persistence to analyze the return and volatility of the cryptocurrency market. The experiment used daily data for more than two years to test the long memory and market efficiency characteristics of the cryptocurrency market. The author uses the logarithmic cycle diagram regression method to study the stability of the cryptocurrency market, and uses the ARFIMA-FIGARCH model to test the long memory behavior of cryptocurrencies in time and scale. Generally speaking, experiments show that in 8 cryptocurrency markets, using full-time and cross-scale daily data (from August 25, 2015 to March 13, 2018), there are heterogeneous memory behaviors.

Portfolio of cryptocurrency assets

Research on cryptocurrency pairs and related factors

Ji et al. used the return and volatility spillovers of six large cryptocurrencies (collected from the coinmarketcap list from August 7, 2015 to February 22, 2018) to test connectivity, and found that Litecoin and Bitcoin are against other cryptocurrencies. Currency has the greatest impact. The author followed the method of Diebold et al. to establish a network of positive/negative returns and volatility connectivity. In addition, regression models are used to identify the drivers of the integration level of various cryptocurrencies. Further analysis shows that the relationship between the yield and volatility of each cryptocurrency is not necessarily due to its market size. Adjepong et al. discussed the market consistency and volatility causality of seven major cryptocurrencies. The method based on wavelet transform is used to test market connectivity. Using parametric and non-parametric tests to study the direction of asset volatility spillover. The experiment revealed the connection of the cryptocurrency market from diversified returns to connectivity and volatility. Elie et al. found that jumps were detected in a series of 12 cryptocurrency returns, and significant jumps were found in all cases. More results emphasize the importance of the jump in transaction volume for the formation of the jump in cryptocurrency.

Some researchers have explored the relationship between cryptocurrency and different factors, including futures, gold, etc. Hale et al. believe that after CME issues futures that are consistent with pricing dynamics, the price of Bitcoin will rise rapidly And fell. Specifically, the author pointed out that the rapid rise and subsequent decline in prices after the launch of futures is consistent with trading behavior in the cryptocurrency market. Werner et al. focused on the asymmetric correlation between major currencies and cryptocurrencies. The results of multifractal asymmetric detrending cross-correlation analysis show that the cross-correlation between most cryptocurrency pairs and ETF pairs has significant persistence and asymmetric multiplicity. Bai et al. studied foreign exchange trading algorithms in the cryptocurrency market using the automatic triangular arbitrage method. Realizing pricing strategies, realizing trading algorithms and developing given trading simulations are the three problems to be solved in this research. Kang et al. used dynamic conditional correlations (DCCs) and wavelet coherence to analyze the hedging and diversification characteristics of gold futures relative to Bitcoin prices. The DCC-GARCH model is used to estimate the time-varying correlation between Bitcoin and gold futures. Through the modeling of variance and covariance, these two flexibility are also considered. The wavelet coherence method pays more attention to the cooperative movement between Bitcoin and gold futures. The experimental results show that the wavelet coherence analysis results show that there is volatility persistence, causality and phase difference between Bitcoin and gold. Dyhrberg et al. applied the GARCH model and the exponential GARCH model to analyze the similarities between Bitcoin, gold and the US dollar. Experiments have shown that Bitcoin, Gold, and the U.S. dollar have similarities with the variables of the GARCH model, have similar hedging capabilities, and respond symmetrically to good news and bad news. The author observes that Bitcoin can combine some of the advantages of commodities and currencies in the financial market and become a tool for portfolio management. Baur et al. extended the research of Dyhrberg et al.; tested the same data and sample period with GARCH and EGARCH-(1,1) models, but the experiment reached different conclusions. Baur et al. found that Bitcoin has unique risk-return characteristics compared with other assets. They noticed that Bitcoin’s excess returns and volatility compared to gold or the U.S. dollar resembled a highly speculative asset. Bouri et al. used DCCs and GARCH (1, 1) The model studies the relationship between Bitcoin and energy commodities. In particular, the research results show that Bitcoin is a powerful hedge and safe haven for energy commodities. Kakushadze proposed a factor model for the cross-section of daily crypto asset returns, and provided source code for data download, calculation of risk factors and backtesting of all cryptocurrencies and a large number of other digital assets. The research results show that for effective execution and shorting of encrypted assets, cross-sectional statistical arbitrage trading is possible. Beneki et al. tested the hedging ability between Bitcoin and Ethereum through the multivariate BEKK-GARCH method and impulse response analysis in the VAR model. The results show that there is volatile trading between Ethereum and Bitcoin, which means that there may be profitable trading strategies in the cryptocurrency derivatives market. Guglielmo et al. studied the weekly effect of the cryptocurrency market and discussed the feasibility of this indicator in trading practice. Student t-test, ANOVA, Kruskal–Wallis, and Mann–Whitney tests were performed on cryptocurrency data to compare time periods that may have abnormal characteristics with other time periods. When an abnormality is detected, an algorithm is built to take advantage of profit opportunities (MQL4 MetaTrader terminal is mentioned in this research). The results show that through the 2013-2016 backtest, there is an abnormality in the Bitcoin market (abnormal positive returns on Monday) t test, ANOVA, Kruskal–Wallis, and Mann–Whitney test in order to compare time periods that may have abnormal characteristics with other time periods. When an abnormality is detected, an algorithm is built to take advantage of profit opportunities (MQL4 MetaTrader terminal is mentioned in this research). The results show that through the 2013-2016 backtest, there is an abnormality in the Bitcoin market (abnormal positive returns on Monday) t test, ANOVA, Kruskal–Wallis, and Mann–Whitney test in order to compare time periods that may have abnormal characteristics with other time periods. When an abnormality is detected, an algorithm is built to take advantage of profit opportunities (MQL4 MetaTrader terminal is mentioned in this research). The results show that through the 2013-2016 backtest, there is an abnormality in the Bitcoin market (abnormal positive returns on Monday)

Research on Crypto Asset Portfolio

Some researchers apply portfolio theory to encrypted assets. Corbet et al. conducted a systematic analysis of cryptocurrency as a financial asset. Brauneis et al. applied the Markowitz mean-variance framework to evaluate the risk return of cryptocurrency investment portfolios. In an out-of-sample analysis of transaction costs, they found that combining cryptocurrencies can enrich investment opportunities in "low-risk" cryptocurrencies. In terms of Sharpe ratio and certainty equivalent returns, the 1∕n-portfolio (i.e., "naive" strategy, such as dividing evenly between asset classes) outperforms a single cryptocurrency, and the mean-variance optimal portfolio In terms of Sharpe ratio and certainty equivalent returns, more than 75%. Castro et al. developed a portfolio optimization model based on the Omega measurement, which is more comprehensive than the Markowitz model, and applied it to four encrypted asset portfolios through numerical applications. Experiments show that encrypted assets increase the return on investment portfolios, but on the other hand they also increase risk exposure.

Brady et al. studied the diversification ability of Bitcoin in the global investment portfolio of six asset classes from the perspective of investors trading five major fiat currencies (ie, US dollar, British pound, euro, Japanese yen, and RMB) . They used the modified conditional value-at-risk and standard deviation as risk measures to optimize the portfolio of three asset allocation strategies, and provided insights into the huge differences in currency Bitcoin trading volume from the perspective of portfolio theory. Antipova et al. also conducted a similar study, exploring the possibility of diversifying investments by using one or more cryptocurrencies, and evaluating investors’ returns based on risks and returns, thereby establishing and optimizing global investment portfolios . Fantazzini et al. proposed a set of models that can be used to estimate the market risk of a cryptocurrency portfolio, while using a zero price probability (ZPP) model to estimate its credit risk. The results show that the prediction of market risk by t-copula/skewed-t-GARCH model is better than the prediction of credit risk by ZPP model. Qiang et al. studied the common dynamics of Bitcoin exchange. They used a connectivity indicator based on the actual daily volatility of the Bitcoin price and found that Coinbase is undoubtedly the market leader, while Binance's performance is surprisingly weak. The research results also show that, relative to transaction volume, safer asset extraction is more important for the volatility link between Bitcoin exchanges.

Trucios et al. proposed a method based on vine copulas and robust volatility models to estimate the value at risk (VaR) and expected gap (ES) of cryptocurrency portfolios. The algorithm shows good performance in VaR and ES estimation. Hrytsiuk et al. proved that the rate of return of cryptocurrency can be described by the Cauchy distribution, obtained the analytical expression of VaR risk measurement, and performed corresponding calculations. As a result of optimization, a set of optimal cryptocurrency investment portfolios were established in their experiments.

Jiang et al. proposed a two-hidden-layer CNN that takes the historical price of a group of cryptocurrency assets as input and outputs the weight of the group of cryptocurrency assets. This research focuses on the use of emerging technologies such as CNN in the portfolio research of cryptocurrency assets. Training is performed in an intensive manner to maximize the cumulative return, which is considered to be the reward function of CNN. The performance of the CNN strategy is compared with three benchmarks and three other portfolio management algorithms (buy-and-hold strategy, unified constant rebalancing portfolio, and universal portfolio based on online Newton step and passive-active mean regression), The results show that the performance of the CNN strategy is positive, and the performance of the model is second only to the aggressive mean regression algorithm (PAMR) of the passive mean regression algorithm. Estalayo et al. reported preliminary findings about the combination of DL model and Multi-Objective Evolutionary Algorithm (MOEA) used to allocate cryptocurrency portfolios. The paper gives the technical principles and details of the superimposed DL recurrent neural network design, and how to use its predictive ability to accurately estimate the returns and risks of the investment portfolio in advance. A set of experimental results on real cryptocurrency data verified the superior performance of the deep learning model they designed compared to other regression techniques.

Research on market conditions

Foam and collision analysis

Phillips and Yu proposed a method to test the existence of a cryptocurrency bubble, which was extended by Shaen et al. This method is based on the supremum augmented Dickey-Fuller (SADF), which tests for bubbles by including a series of forward recursive right-tailed ADF unit root tests. In addition, an extended methodological generalized SADF (GSAFD) test was performed on bubbles in cryptocurrency data. The conclusion of this study is that there is no clear evidence that there is a persistent bubble in cryptocurrency markets such as Bitcoin or Ethereum. Bouri et al. date stamped the price explosion of seven large cryptocurrencies and revealed evidence of the explosion in multiple periods in all cases. GSADF is used to identify multiple explosion periods, and logistic regression is used to reveal the co-explosive evidence of cryptocurrencies. The results show that the possibility of a cryptocurrency's explosive period usually depends on the explosive existence of other cryptocurrencies, and points to the co-explosiveness of the same period, not necessarily depending on the size of each cryptocurrency.

The extended study of Phillips et al. and Landsnes et al.(they applied the recursively enhanced Dickey-Fuller algorithm, called the PSY test) studied the possible predictors of certain cryptocurrency bubble periods. The assessment includes multiple bubble periods for all cryptocurrencies. The results show that higher volatility and trading volume are positively correlated with the existence of cryptocurrency bubbles. In terms of bubble prediction, the author found that the probit model performed better than the linear model.

Phillips et al. used Hidden Markov Model (HMM) and Ranking of Advantages and Disadvantages (SIR) to identify bubble behavior in the time series of cryptocurrencies. Combining HMM and SIR methods, introducing an epidemic detection mechanism into social media to predict cryptocurrency price bubbles. Experiments have proved that there is a strong relationship between the use of Reddit and the price of cryptocurrencies. This work also provides some empirical evidence that bubbles reflect social epidemics, such as the spread of investment ideas. Guglielmo et al. studied price overreaction in cryptocurrency transactions. Some parametric and non-parametric tests confirmed the existence of price patterns after overreaction, indicating that the price changes in both directions on the second day were greater than the price changes after the "normal" day. The results also show that the overreaction detected in the cryptocurrency market does not provide usable profit opportunities (perhaps due to transaction costs) and cannot be considered as evidence of the efficient market hypothesis. Chaim et al. analyzed the high unconditional volatility of cryptocurrencies, from the standard lognormal random volatility model to discontinuous jumps in volatility and returns. This experiment shows the importance of incorporating permanent jumps into volatility in the cryptocurrency market.

Extreme conditions

Unlike traditional fiat currencies, cryptocurrencies have higher risks and exhibit heavier tail behavior. Paraskevi et al. found that there is an extreme dependence between the rate of return and transaction volume. The experiment also found that due to the difference in the correlation between the positive and negative excess returns of all cryptocurrencies, there is an asymmetric return-volume relationship in the cryptocurrency market.

The price of cryptocurrency plummeted from the end of 2017 to the beginning of 2018. Yaya et al. studied the persistence and dependence of Bitcoin on other popular alternative currencies before and after the collapse of the cryptocurrency market in 2017/18. The results show that due to the speculative psychology of cryptocurrency traders, it is expected that the duration of the shock after the crash will be higher, and there will be more evidence of non-mean reversion, which means that the price of cryptocurrency may fall further.

Other related to cryptocurrency transactions

Some other research papers related to cryptocurrency trading mainly focus on market behavior, regulatory mechanisms and benchmarks.

Krafft et al. and Yang respectively analyzed market dynamics and abnormal behavior to understand the impact of market behavior in the cryptocurrency market. Krafft and others discussed the potential final causes, potential behavioral mechanisms, and potential regulatory context factors to enumerate the possible impact of GUI and API on the cryptocurrency market. Then, they emphasized the potential social and economic impact of human-computer interaction in digital agency design. On the other hand, Yang used the behavioral theory of asset pricing anomalies and tested 20 market anomalies using cryptocurrency transaction data. The results show that anomalous research pays more attention to the role of speculators, which provides new ideas for studying the momentum and reversal of the cryptocurrency market. Cocco et al. implemented a mechanism to form bitcoin prices and specific behaviors for each type of trader, including initial wealth distribution following Pareto's law, order-based transactions, and price settlement mechanisms. Specifically, the model reproduces the unit root property of price series, thick tail phenomenon, volatility clustering of price returns, Bitcoin generation, hash power and power consumption.

Leclair and Vidal Thomás et al. analyzed the existence of herding behavior in the cryptocurrency market. Leclair used Huang and Salmon's grazing method to estimate market herd dynamics under the CAPM framework. Vidal Thomás et al. analyzed whether there are groups in the cryptocurrency market by returning to the cross-sectional standard (absolute) deviation. Their research results all show important evidence of herding effect in the cryptocurrency market. Makarov et al. studied the price impact and arbitrage dynamics in the cryptocurrency market and found that the 85% Bitcoin return rate change and the special component of the order flow played an important role in explaining the size of the arbitrage spread between exchanges.

In November 2019, Griffin and others proposed a paper on unsupported digital money/unsupported digital money raising the price of cryptocurrency, which caused a great sensation in academia and public opinion. Using algorithms to analyze blockchain data, they found that Tether purchased large amounts of Bitcoin during the market downturn, which caused the price of Bitcoin to rise sharply. By drawing the blockchain diagram of Bitcoin and Tether, they were able to determine that a large player on Bitfinex used Tether to buy a large amount of Bitcoin when the price fell.

More research involves the benchmarks and development of the cryptocurrency market, regulatory framework analysis, data mining techniques in cryptocurrency trading , and the application of the efficient market hypothesis in the cryptocurrency market, and research on the artificial financial market of the cryptocurrency market. Hileman et al. divided the cryptocurrency industry into four key industries: exchanges, wallets, payments, and mining. They conducted benchmark research on individuals, data, regulation, compliance practices, and company costs, and drew a global mining map of the cryptocurrency market in 2017. Zhou et al. discussed the status and future of computer trading in the largest economy in the Asia-Pacific region, and then also considered algorithms and high-frequency trading in the cryptocurrency market. Shanaev et al. used the data of 120 regulatory events to study the meaning of cryptocurrency supervision, and the results showed that stricter supervision of cryptocurrencies is not advisable. Akhilesh et al. used the average absolute error calculated between the actual value and the predicted value of the market sentiment of different cryptocurrencies on the day as a method of quantifying uncertainty. They use the comparison of uncertainty quantitative methods and opinion mining to analyze current market conditions. Sigaki et al. used permutation entropy and the statistical complexity of the sliding time window returned by the price log to quantify the dynamic efficiency of more than 400 cryptocurrencies. Therefore, the cryptocurrency market exhibits significant consistency with the efficient market hypothesis. Cocco et al. described an agent-based artificial cryptocurrency market in which heterogeneous agents buy and sell cryptocurrencies. The proposed simulator can reproduce some real statistical characteristics of price returns observed in the real Bitcoin market. Marko considered the future use of cryptocurrency as currency based on the long-term value of cryptocurrency. Neil et al. analyzed the influence of network effects on competition in the new cryptocurrency market. Bariviera and Merediz-Sola conducted a survey based on hybrid analysis, proposed a methodological hybrid approach for comprehensive literature review, and provided the latest technology in the cryptocurrency economics literature.

There are also some studies and papers that introduce the basic processes and rules of cryptocurrency transactions, including Hansel et al., Kate, Garza et al., Ward et al., and Fantazzini et al. Research results. Hansel et al. [124] introduced the basics of cryptocurrency, Bitcoin and blockchain, methods of identifying market profit trends, methods of using Altcoin trading platforms (such as GDAX and Coinbase), and using encrypted wallets to store and protect coins in the ledger Methods. Kate et al. set six steps to show how to start investing without any technical skills in the cryptocurrency market. This book is an entry-level trading manual for beginners to learn cryptocurrency trading. Garza et al. simulated an automatic cryptocurrency trading system to help investors limit systemic risks and increase market returns. This article is an example of designing an automatic cryptocurrency trading system. Ward et al. discussed algorithmic cryptocurrency trading using several general algorithms and modified them, including adjusting the parameters used in each strategy, as well as mixing multiple strategies or dynamically changing between strategies. This article is an example of algorithmic trading in the cryptocurrency market. Fantazzini et al. introduced R package Bitcoin finance and bubbles, including financial analysis of cryptocurrency markets including Bitcoin.

Regarding the community resource of cryptocurrency and blockchain, the academic exchange platform is the "blockchain research network".

Summary analysis of literature review

Analyzed the timing of research, the distribution of research in technical methods, and the distribution of research in attributes. This article also summarizes the data sets used in cryptocurrency trading research.

Timeline

Figure 8 shows several major events in cryptocurrency trading. This timeline contains milestones in cryptocurrency trading and important scientific breakthroughs in this field.

As early as 2009, Satoshi Nakamoto proposed and invented the first decentralized cryptocurrency Bitcoin. It is considered the beginning of cryptocurrency. In 2010, the first cryptocurrency exchange was established, which means that cryptocurrency will no longer be an over-the-counter market, but will be traded on an exchange based on the auction market system.

In 2013, Kristoufek concluded that there is a strong correlation between the price of Bitcoin and the frequency of "Bitcoin" search queries in Google Trends and Wikipedia. In 2014, Lee and Yang first proposed the causality test based on copula in the quantile method from the transaction volume of seven major cryptocurrencies to the rate of return and volatility.

In 2015, Cheah et al. discussed the bubble and speculation of Bitcoin and cryptocurrencies. In 2016, Dyhrberg used the GARCH model combined with gold and the U.S. dollar to study the volatility of Bitcoin.

From the end of 2016 to 2017, apply machine learning and deep learning techniques to the prediction of cryptocurrency returns. In 2016, McNally et al. used the LSTM algorithm to predict the price of Bitcoin. Bell and Zbikowski et al. applied SVM algorithm to predict the trend of cryptocurrency prices. In 2017, Jiang et al. used a dual-Q network and used DBM to pre-train it to predict the weight of the cryptocurrency portfolio.

In recent years, in the field of cryptocurrency trading, several research directions have been considered, including cross-asset portfolio, transaction network applications, and machine learning optimization.

Research the distribution of attributes

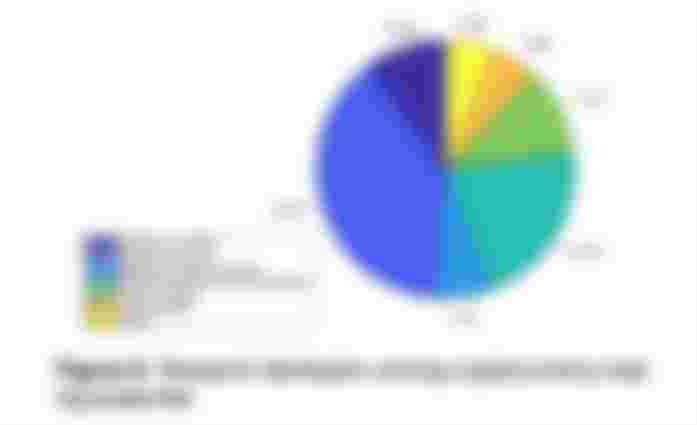

We counted the number of papers covering different aspects of cryptocurrency trading. Figure 9 shows the results. The attributes in the legend are arranged according to the number of papers that specifically test the attributes.

More than one-third (38.10%) of the thesis research earnings forecast. Another third of the papers focused on the study of bubbles and extreme conditions in cryptocurrency trading and the relationship between pairings and portfolios. The remaining research topics (volatility prediction, trading systems, technical trading, etc.) account for about one-third of the share.

Research distribution between categories and technologies

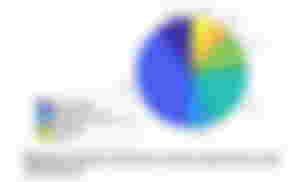

This section introduces and compares the types and technologies of cryptocurrency transactions. When the paper involves multiple technologies or compares different methods, we draw statistics from different technical perspectives. Of the 126 papers, 87 (69.05%) involved statistical methods and machine learning. These papers mainly study the technical level of cryptocurrency trading, including mathematical modeling and statistics. Other papers related to pure technical indicator trading systems and papers describing the industry and its history are not included in this analysis. Among 87 papers, 75 (86.21%) introduced statistical methods and techniques in cryptocurrency trading research, and 13.8% of the papers studied the application of machine learning in cryptocurrency trading (see Figure 10). It is worth mentioning that 16 papers (18.4%) applied and compared multiple technologies in cryptocurrency transactions. More specifically, Bach et al. , Alessandretti et al., Vo et al., Phaladisialoed et al., Siaminos et al. [222], Rane et al. in cryptocurrency transactions Statistical methods and machine learning methods are used in.

Table 7 shows the search results of all trading areas (not limited to cryptocurrencies). From the table, we can see that most of the research results focus on statistical methods in trading, which means that most research on traditional markets is still focused on using statistical methods for trading. But we have observed that machine learning pays more attention to transactions. This may be because traditional technology and fundamentals have been arbitrage, so the market has been looking for new anomalies to take advantage of. At the same time, the research results also show that there are many research opportunities in the field of widely studied machine learning applied to cryptocurrency market transactions.

Research distribution of statistical methods

As shown in Figure 10, we use statistical methods to further divide the papers into 6 categories:

(i) basic regression methods.

(ii) linear classifiers and clustering.

(iii) time series analysis.

(iv) decision trees and probabilistic classification.

(V) Modern portfolio theory & Others.

Basic regression methods include regression methods (linear regression), function estimation and CGCD methods. Linear classifiers and clustering include SVM and KNN algorithms. Time series analysis includes GARCH model, BEKK model, ARIMA model, wavelet time scale method. Decision trees and probability classifiers include Boosting trees and RF models. Modern portfolio theories include value-at-risk theory, expected gap theory, Markowitz mean-variance framework, etc. Others include industry, market data and research analysis of the cryptocurrency market.

The figure shows that basic regression methods and time series analysis are the most commonly used methods in this field.

Research on Machine Learning Classification Distribution

Papers using machine learning accounted for 22.78% of the total (cf Figure 10). We further divide these papers into three categories: (vii) ANNs (viii) LSTM/RNN/GRUs and (ix) DL/RL.

The figure also shows that methods based on LSTM, RNN and GRU are the most popular in this sub-field.

Artificial neural networks include papers that study the application of artificial neural networks in cryptocurrency transactions, such as back propagation (BP) neural networks. LSTM/RNN/GRUs include papers using neural networks, using the time structure of data, which is a technology particularly suitable for time series forecasting and financial transactions. DL/RL includes papers using multilayer neural networks and reinforcement learning. The difference between ANN and DL is that in general, DL refers to an ANN with multiple hidden layers, and ANN refers to a neural network with a simple structure including an input layer, hidden layer(s) and an output layer.

Data sets used in cryptocurrency transactions

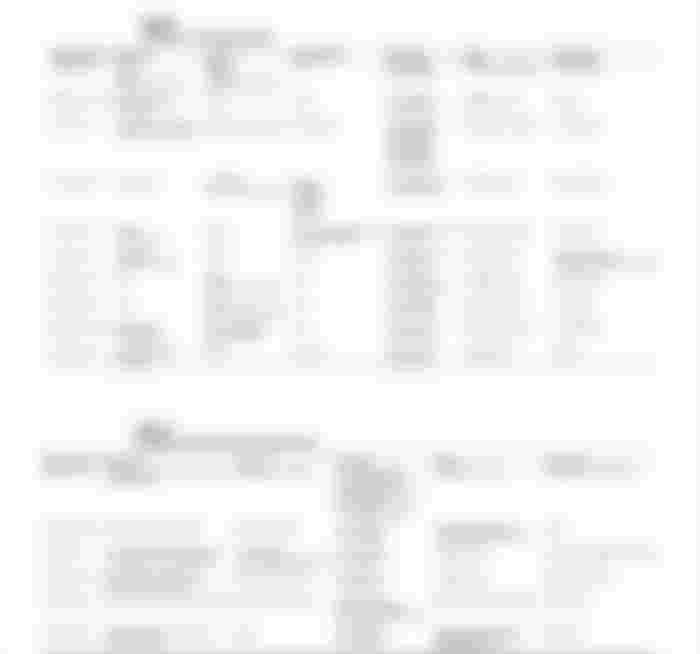

Table 8-10 shows the details of some representative data sets used in cryptocurrency trading research. Table 8 shows the market data set. They mainly include price, transaction volume, and order level information collected from cryptocurrency exchanges. Table 9 shows data based on emotions. Most of the data sets in this table contain market data and media/Internet data with emotional or statistical labels. Table 10 gives two examples of data sets used in collected papers not covered in the first two tables.

The "Currency" column shows the type of cryptocurrency; this indicates that Bitcoin is the most commonly used currency in cryptocurrency research. The "Description" column shows the general description and type of the data set. The "data resolution" column indicates the delay time of the data (for example, used in backtesting)-this helps distinguish between high-frequency trading and low-frequency trading. The "Time Range" column shows the time span of the data set used in the experiment; this makes it easy to distinguish between current performance and long-term impact in a specific time interval. We also introduced how to use the data set (ie task), see the "Usage" column. The "data source" details where to retrieve the data, including cryptocurrency exchanges, aggregate cryptocurrency indexes, and user forums (for sentiment analysis).

Alexander et al. also investigated cryptocurrency data. They summarized the data collected from 152 published cryptocurrency papers discussed with SSRN and analyzed their data quality. They found that since January 2017, less than half of cryptocurrency papers used correct data.

Opportunities for cryptocurrency trading research

This section discusses potential future research opportunities for cryptocurrency trading.

Research based on emotions.

As mentioned above, there is a lot of work using natural language processing technology for sentiment analysis. The ultimate goal is to use news and media content to improve the performance of cryptocurrency trading strategies.

Possible research directions may include: adding a large number of media inputs in sentiment analysis (for example, adding video sources); updating the baseline natural language processing model to perform more robust text preprocessing; applying neural networks in label training; during the retention period Expansion of the sample; transaction costs; and, user reputation research.

Long-term and short-term research .

In cryptocurrency trading, there are significant differences in the short and long term. In long-term trading, investors may obtain greater profits, but when managing positions in weeks or months, there are more possibilities to control risks. Due to the increase in the holding period, the risks of long-term strategies must be controlled, which is proportional to the risks borne by traders. On the other hand, the longer the term, the higher the risk, and the most important thing is risk control. The shorter the period, the higher the cost, and the lower the risk, so the cost occupies the dominant position in the strategic design. In short-term trading, when the holding period is less than one week, automatic algorithm trading can be applied. By applying wavelet techniques to analyze the bubble mechanism, and considering the price explosion assumptions for short-term and long-term research, researchers can distinguish long-term and short-term transactions in cryptocurrency transactions.

The existing work is mainly about the difference between long-term and short-term cryptocurrency transactions. Long-term trading means less time required for simple technical indicators in trend tracking and market analysis. Short-term trades can limit the overall risk because each trade uses a small position. However, market noise (interference) and short trading hours may cause short-term trading pressure. It may also be an interesting topic to explore the extraction of trading signals, time series research, applications in portfolio management, the relationship between market crashes and small price drops, and the pricing of derivatives in the cryptocurrency market.

The relevance of cryptocurrency to other currencies. Since monetary policy and business cycles are not controlled by the central bank, cryptocurrencies are always negatively correlated with overall financial market trends. There have been some studies discussing the correlation between cryptocurrency and other financial markets, which can be used to predict the direction of the cryptocurrency market.

Considering the characteristics of cryptocurrency, the relevance of cryptocurrency and other assets needs further study. Through principal component analysis, the relationship between cryptocurrency and other currencies under extreme circumstances (ie, financial collapse) may achieve a breakthrough.

Bubble and collapse research.

In order to discuss the high volatility and high rate of return of cryptocurrency, current research focuses on the bubble in the cryptocurrency market, the correlation between the cryptocurrency bubble and the volatility index (VIX) and other indicators (this is A "panic index" that measures the implied volatility of S&P 500 index options), the spillover effect of the cryptocurrency market.

Further research on bubbles and collapses in cryptocurrency trading can include the connection between the bubble generation process and financial collapse, and conduct coherence analysis (analysis of the coherence process from bubble formation to bubble bursting consequence analysis), and microeconomics Analysis of bubble theory, try other physical or industrial models (ie Omori’s Law when analyzing the cryptocurrency market bubble, discuss the supply and demand relationship of cryptocurrencies in the bubble analysis (such as using a supply and demand diagram to simulate the generation of a bubble, and simulate the bursting of a bubble ).

Game theory and agent-based analysis.

The application of game theory or agency-based models to transactions is a research hotspot in traditional financial markets. It may also be interesting to apply this method to transactions in the cryptocurrency market.

The publicity of blockchain technology.

In recent years, research on the relationship between the formation of a specific currency transaction network and its price has increased rapidly; the increasing attention to user identification also strongly supports this direction. Through in-depth understanding of these networks, we may discover new features in price predictions, and may be closer to understanding financial bubbles in cryptocurrency transactions.

Study the balance between the opening of the literature and the decline of Alphas. Mclean et al. pointed out that investors learned about mispricing in the stock market from academic publications. Similarly, the predictability of the cryptocurrency market may also be affected by research papers in this field. One possible attempt is to try new pricing methods that apply real-time market changes. Considering that the proportion of informed traders in the cryptocurrency market continues to increase during the pricing process, this is another breakthrough point (finding a balance between alpha trading and trading research literature).

We have conducted a comprehensive overview and analysis of the research work of cryptocurrency trading. This survey proposed a definition of terms and the current state of technology. This article conducts a comprehensive survey of 126 cryptocurrency trading papers and analyzes the characteristics of the research distribution of cryptocurrency trading literature. We further summarized the data set used for the experiment and analyzed the research trends and opportunities of cryptocurrency trading.

We hope that this survey will be useful to both academics (such as financial researchers) and quantitative traders. This survey represents a way to quickly become familiar with the cryptocurrency trading literature, which can incentivize more researchers to contribute to the pressing issues in the field, for example, in accordance with the ideas we have identified.

Conclusion

We have conducted a comprehensive overview and analysis of the research work of cryptocurrency trading. This survey proposed a definition of terms and the current state of technology. This article conducts a comprehensive survey of 126 cryptocurrency trading papers and analyzes the characteristics of the research distribution of cryptocurrency trading literature. We further summarized the data set used for the experiment and analyzed the research trends and opportunities of cryptocurrency trading.

I hope this article will be useful to both academics (such as financial researchers) and quantitative traders. This article represents a way to quickly become familiar with the cryptocurrency trading literature, which can incentivize more researchers to contribute to the pressing issues in the field, for example, in accordance with the ideas I have identified.

Thanks for the information