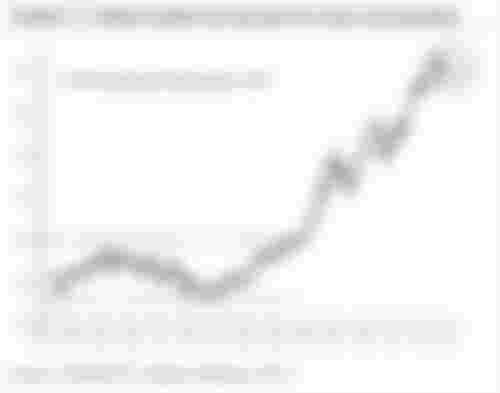

Bank of America’s Target for the S&P 500

We are about to enter the 2020s with a record 90% of Global Fund Manager Survey investors saying the global economy is late cycle. This is because we leave the 2010s stuck in an economic regime characterized by low growth and low inflation. Real GDP has averaged just 2% in the US, 1% in the EU and Japan, and halved from 12% to 6% in China as the world's most populous nation rebalances towards a consumer rather than export-led economy. This is despite historic levels of monetary accommodation since 2009: 768 central bank cuts, US$12.4tn of financial asset purchases and interest rates at 5,000-year lows.

As BofA notes in a recent report, "the combination of globalization, lower interest rates and a policy and macro backdrop of maximum liquidity and minimal growth have served to exacerbate wealth inequality, and create a surplus of global savings relative to investment, i.e. extremely low "animal spirits". Higher debt has also failed to deliver higher growth (note corporations and governments global debt up from US$105tn in 2008 and US$255tn in 2019)."

nstead, the record debt load enabled by the monetary policy largesse of the 2010s has induced significant upside (and polarization) in asset prices, but the economic spoils went to holders of capital not workers. A portfolio of bonds and stocks rose from US$100 to US$223, while US$100 of wages rose to US$125. Reliance on monetarism has also meant modern economic expansions are now driven by booms and busts in financial cycles.

[bad iframe src]

[bad iframe src]

And according to most market watchers, the trends that started in the 2010s are set to continue into the 2020s. Yet ironically, even as debates rage if the US will enter a recession next year, central banks are acting as if a full-blown financial crisis has already erupted. As Bank of America observes, the past 6 months have seen 51 rate cuts, the most since the Global Financial Crisis, meaning "central banks are cutting like it's a crisis."

And with no less than $700 billion (and potentially much more) of G4 central bank QE expected in 2020, a potential economic crisis is precisely what the doctor ordered for the stock market. The result: an S&P which is trading just shy of 3,200 as of this moment, and which BofA's expects to melt up in the first quarter of 2020.

As BofA's Chief Investment Strategist, Michael Hartnett, writes, "the market is primed for a Q1 2020 risk asset melt-up" as i) Fed & ECB are still adding liquidity, ii) the two main global macro risks, Brexit and a Phase One US-China trade deal, appear to have been resolved for the time being, in the process removing lingering USD & 10Y TSY risk premiums. As a result, BOfA expects returns to be front-loaded in 2020, with the S&P500 hitting 3,333 by March 3rd, and the 10Y Treasury rising to 2.2% by 2/2 (Feb 2).

Is there anything on the horizon that can spoil this late cycle melt-up fun for the bulls? Just one thing according to BofA:

As Hartnett writes, "the biggest vulnerability for markets in the 2020s will come from today's bond market bubble: >US$13tn negative yielding debt (of which c.US$1tn corporate), negative German/Swiss curves, Austria 100-year bond yields <1%, global bond yields just off record lows of only 19bp."

Whether it is in 2020, or in the coming years, a policy mistake (inflation targeting/MMT) and/or the start of policy impotence (central banks pushing on a string) "will likely cause a jump in interest rate volatility, end the decade-long bullish combo of minimum rates-maximum profits, and signal the big top in asset prices", according to Hartnett.

It is this disorderly rise in bond yields that would "likely cause extreme pain" as Wall Street deleverages, inevitably leading to pain quickly thereafter for the real economy. This is why the Fed policy pivot on weak credit markets was so aggressive in December 2018/January 2019, and is why Powell is now on hold indefinitely as the Fed prepares to unveil its "symmetric" policy revision, where even inflation rates of 3% or higher will not be sufficient for the US central bank to hike rates. In fact, it is unclear what, if anything, can force the Fed to ever again tighten financial conditions after the bull market's near death experience in Q4 2018.

And yet, central planning inevitably always fails, and it is time to start thinking what the policy response will be to the next recession, which according to BofA will "seek to correct the excesses of the 2010s that led to widespread wealth inequality and financial engineering"... which we doubt, but here goes anyway:

Corporate sector leverage: global corporate debt has risen by 62% 2008-18.

Wall St too big to fail: US private sector financial assets at record 5.6x GDP

Private equity: private equity and venture capital AUM to reach US$4.2tn with 2019 on track to be a new record for fundraising (US$624bn) and AUM a record 5.3% of global equity market cap.

Share buybacks: since 2009, US corporates have spent US$5.4tn on stock buybacks (US corporates have spent US$114 on buybacks since 2018 for every US$100 invested in the real economy vs US$60 from 1998-2017) and issued US$15.0tn debt.

Shadow banking assets: US$28.1tn (in 2010) to US$45.2tn (61%), not including US$2.8tn of private equity assets; shadow banking assets = 73% of global GDP.

Zombie companies: the number of OECD zombie companies (those with an interest coverage ratio below 1) is at new post-GFC highs (548).

As BofA concludes, electorates are already voting for War on Inequality policies and the 2020 US election is likely to be framed as Protectionist (Trump) vs Keynesian (Biden) vs Redistributionist (Sanders/Warren). While Trump is likely to win the 2020 election, the even greater wealth inequality that will be unleashed in the 2020-2024 period virtually assures a progressive/socialist/redistributionist agenda wins in 2024.

BofA also believes that upcoming policy actions will also involve higher US taxes in the 2020s, coupled with "Occupy Silicon Valley" policies to target tech profits, regulation of stock buybacks and a combination of rental price controls, living wages, and student debt forgiveness financed by wealth taxation. If necessary - and it will be - governments will begin to issue debt (MMT) until inflation rises, and eventually culminates in hyperinflation to wipe away the world's untenable debt load.