Checkmate: The Fall of FTX

This essay was originally posted on Heretic Speculator 11/11/22

This morning we've seen the news that crypto exchange FTX has started Chapter 11 bankruptcy proceedings. This is a fitting end to what has been an absolute roller coaster ride of a week in the cryptocurrency industry. A week that started with rumors that FTX might be insolvent. Rumors that were quickly confirmed when Binance and FTX agreed to a letter of intent where Binance would acquire FTX and bail out the company’s obligations. Binance backed out about a day later after assessing FTX’s financials. And that brings us to today; reports of Chapter 11. All in one week. If you had an account with FTX and were on vacation, you may have never had a chance. Your funds are probably gone. Another incredible black eye for an industry that has been purging froth for an entire calendar year. In this essay, we’ll dive into why this happened, what the trigger was, and why the trigger was probably pulled.

Before we get too far into this, I want to explicitly make it clear that some of what you’re about to read is speculation. While there are numerous factual pieces of information throughout this story, some of the key takeaways are pure conjecture. But I believe there is enough connecting many of these details that when presented together we can reasonably assume the conclusions.

The Players

What we’re witnessing with the collapse of FTX is arguably one of the most significant developments in crypto’s history. In my view, this is bigger than the Tornado Cash sanctions, bigger than the Celsius Network bankruptcy, bigger than the collapses of Terra, Voyager, or 3 Arrows Capital. What is happening with FTX is bigger because of who it takes down and what that person had spent so much time doing before his professional demise.

Sam Bankman-Fried, or SBF as he’s known in the community, was viewed as one of the biggest giants in the industry. Crypto gets a lot of flak from the traditional finance community for being a largely unregulated casino but I don’t think anybody can debate that crypto is big business in 2022 and that business has produced numerous billionaires.

At the top of that billionaires list is Binance founder Changpeng “CZ” Zhao. Just beneath him is Bankman-Fried. Coinbase founder Brian Armstrong and the Winklevoss twins are also among the crypto exchange founder billionaires club. But up until this week, only Zhao was reportedly worth more than Bankman-Fried. CZ remains top dog, SBF was the clear #2, and then it was a long way down to #3 in terms estimated net worth. SBF and CZ were the 11-figure billionaires.

While all of these guys I just mentioned have made fortunes running essentially the same type of centralized crypto exchange businesses, to assume they have the same views on the correct regulatory approach to those businesses would probably be wrong. On one end of the spectrum we have CZ, who has previously faced questions by the US Justice Department over concerns of money laundering on Binance. On the other end we have SBF, who has been actively working with US politicians to build a regulatory framework covering the entire industry.

“I am spending a lot of time talking with members about what constructive things would be on crypto policies and about what can be done to provide federal oversight of it. And so when I go to D.C., that is often what I’m doing. I think that it is really important that there’s federal oversight of the crypto industry.” - Sam Bankman-Fried, FTX

Sam put his money where is mouth is too. He donated tens of millions of dollars to various political interests. As we later learned, that was money that he intended to cash in for favors fairly quickly.

Bad Blood

SBF’s crypto exchange, FTX, has been hard to miss in 2022. The company had an ad in the Super Bowl earlier this year and even sponsored the Miami Heat’s home arena. Tom Brady, Steph Curry, and Shaquille O’Neal were brand ambassadors. The company’s rise was incredibly fast. Founded in 2019, FTX quickly became one of the largest exchanges in the entire crypto industry. One of the only exchanges that was bigger? Changpeng Zhao’s Binance.

Interestingly, CZ and SBF have been connected from the start - Binance occasionally invests in crypto startups and was one of the original investors in FTX. But last year, Binance abruptly pulled it’s equity out of FTX right around the time FTX was closing a $900 million funding round at an $18 billion valuation. CZ told Forbes the exit was all about a “normal investment cycle.”

“We’ve seen tremendous growth from them, we're very happy with that but we’ve exited completely. We're still friends but we no longer have any equity relationship.” - Changpeng Zhao, Binance

Even at the time, this was seen by some as a somewhat strange exit given the messaging from Binance during the announcement of the original investment a couple years prior; where the company mentioned it was a strategic investment to build out the crypto ecosystem together. That seems like something you say when you’re in for the long haul. Two years certainly isn’t the long haul in the private equity world. If SBF was irritated by CZ pulling funds, that frustration may have contributed to comments like this:

Perhaps a playful jab? Doubtful. Judging by the fact that the tweet was deleted, it’s more likely an intentional dig at CZ for not lobbying for crypto regulation the way that SBF did. But there are likely reasons why CZ isn’t taking the same steps that SBF took toward regulation. One could be that he doesn’t need to since he’s already running an incredibly profitable business and has more money than he could possibly spend in 10 lifetimes. Another could be that Changpeng Zhao’s motivations are simply not the same as Sam Bankman-Fried’s.

“It’s worth noting SBF always saw blockchain more as a means to an end. He entered crypto after a few years as a Jane Street quant, with the stated aim of making as much money to gain as much influence as possible.” - Daniel Kuhn, CoinDesk

While the casual viewer might think Sam Bankman-Fried’s fall from crypto grace happened this week, it actually happened several weeks before that. This week is just the week he was officially booted from the community.

The Snake Way

Personal jabs and taunts at an original investor who helped put you on are probably not a good look. But if we take the view that passive aggressive digs like the ones which CZ has seemingly committed as well are harmless, one has to ask what it would take to push a billionaire to decide to destroy an adversary. The presumable answer? Messing with that billionaire’s money by bringing on the heat.

In mid-October, SBF released a long list of policy recommendations for regulators to consider when approaching how best to oversee the cryptocurrency market. While there were some things in the proposal that weren’t totally awful, most of it was. And Sam heard about it from other influential people in the crypto space. Ryan Adams of Bankless took the proposal to task in one tweet. Erik Voorhees eloquently dismantled SBF’s proposal point by point.

Defi transcends humans and their political machinations. Defi operates through immutable code, and as such, represents “an economy of laws and not of men.” It is this neutral, objective foundation for economic arrangement which future generations will look back upon and thank us for. - Erik Voorhees

A cornerstone feature of SBF’s proposal was for all of DeFi to require KYC/AML and licensing. What is DeFi? It is the ability to lend, swap, and borrow without a centralized intermediary. It is Uniswap, AAVE, and Compound. It’s the ability to open any Ethereum wallet application from any software developer and participate on the network as the user sees fit. DeFi is the exact opposite of centralized exchanges. It is computer code with objective rules pertaining to collateralization ratios and liquidation parameters.

DeFi, simply put is financial freedom. Mandating licensure would effectively outlaw DeFi applications entirely. Decentralized exchanges like the ones that make up “DeFi” are in competition with centralized exchanges like FTX. And Sam Bankman-Fried essentially proposed regulating them out of existence. SBF quite literally attempted to buy off politicians and regulators so they would ratify his ideas and destroy his decentralized competitors. While Binance certainly can’t claim to be a decentralized entity, the company does benefit from DeFi through adoption of Binance Coin (BNB-USD); the native token of the second largest smart contract ecosystem behind only Ethereum (ETH-USD). While he operates a centralized exchange, CZ also benefits from the success of DeFi indirectly. Sam did not.

CZ Destroys SBF

It’s not everyday that you see a multibillionaire casually destroy another multibillionaire from the same industry in a matter of just a few days but that’s exactly what Changpeng Zhao just did. How’d he do it exactly? At the end of the day, it was actually pretty simple. As part of Binance’s exit from the FTX investment, CZ had control of a little under $600 million in FTX Token (FTT-USD) that he received in exchange for the equity. Even though CZ no longer had equity in FTX the business, he still had an enormous position in FTX Token.

What is FTX Token?

The FTX Token itself is actually nothing. Like all cryptos (and most dollars at this point as well), FTT is simply numbers on a screen backed by code and faith. FTT was created out of thin air by the FTX team and used, among other things, as the centerpiece of a rewards-based model within the FTX exchange. Some of those rewards included better rates on swaps and the token could also be accrued for providing funding to FTX’s centralized liquidity pool.

Simply put, FTT is the kind of utility token that is very common in the crypto space among the centralized exchanges. Celsius Network (CEL-USD), Nexo.io (NEXO-USD), Crypto.com (CRO-USD), and Voyager Digital (VGX-USD) all have similar platforms and utility token models. What gives these tokens value is the idea they can be used to help the consumer save money in some way when using an exchange. But they’re not interchangeable. You can’t buy VGX and stake it on Crypto.com to get discounts on transactions - you need CRO for Crypto.com. It would be akin to trying to spend a Starbucks gift card at Dunkin’ Donuts.

This means successful platforms can see enormous gains in their utility tokens as well. At one point in late 2021, FTT’s market cap actually hit $9 billion. Reminder, this is just the FTX Token. It isn’t the valuation of the business. But it gives some context into just how extended some of these coins got last year and FTT was no different. The biggest problem for FTT is that it’s a wildly centralized token.

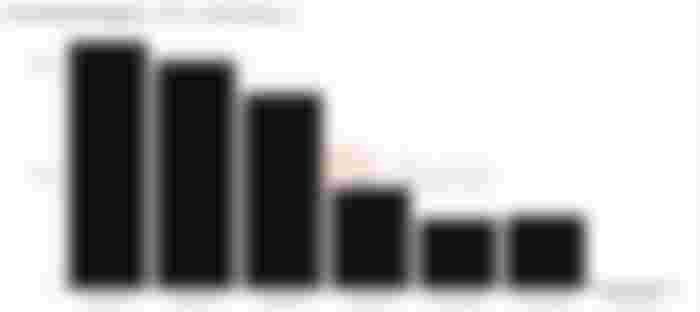

I’ve researched a lot of these coins personally and I can’t recall a level of token concentration as extreme as the one that was seen in FTT. The top 100 token wallet addresses had control of over 99% of the token supply before the meltdown at FTX. While high concentration levels are typical with centralized exchange tokens and alt coins, successful cryptos have much better token distributions. Bitcoin (BTC-USD) is the shining star example; the top 100 token addresses control about 15% of the supply. For something like Dash (DASH-USD) that figure is about 25%. And remember, in the case of FTT one of these top token holders is actually Changpeng Zhao.

The Opportunity

The missing detail that allowed CZ to eviscerate FTX is Sam Bankman-Fried actually owned two multi-billion dollar crypto companies. Alameda Research is the quant trading outfit that SBF built in 2015. Alameda Research and FTX were supposed to be independent operators. As it turned out, they were anything but that and FTX was funneling funds to Alameda Research. Alameda was then putting those funds to work in the crypto market. And when the crypto market turned earlier this year, things got very ugly. A leaked balance sheet by CoinDesk earlier this month showed Alameda had a massive position in FTT - the utility token of sister company FTX.

While there is nothing per se untoward or wrong about that, it shows Bankman-Fried’s trading giant Alameda rests on a foundation largely made up of a coin that a sister company invented, not an independent asset like a fiat currency or another crypto. - Ian Allison, CoinDesk

There was actually so much FTT on Alameda’s balance sheet, that nearly the entire net equity position the company was attributable to its FTT position. Because Alameda Research was using FTT as collateral, a sharp drop in the price of FTT could theoretically wipe out Alameda Research and also have huge implications for FTX as well. All that was needed was the right pin prick.

The day before CZ tweeted his intention to liquidate his FTT position, FTT closed at $24 per coin. On November 6th, the day of the tweet, FTT closed at $22.26. Alameda Research’s CEO telegraphed support for the token at $22, indicating Alameda would buy CZ’s entire position out of market if he was willing to sell at $22. He declined. Suddenly, everyone was concerned about the solvency of Alameda and FTX. And the funds started leaving the FTX exchange.

On November 7th, FTX’s Bitcoin balance on the exchange fell from over 20k BTC down to nothing - a roughly $410 million value at the time. And it wasn’t just Bitcoin.

FTX’s Ethereum token balance plummeted from $2.6 billion on November 5th to just $622 million yesterday. Just an old school bank run but without the paper or the lines. On November 8th, FTT closed at $5.50. As of writing, it’s about $2. FTX and Alameda are now both bankrupt. And all it took to push the scheme over the cliff was a leaked balance sheet and a tweet. Of course, CZ’s power was actually having control of such a large FTT position even when he no longer had interest in the business as an investment. Without his FTT, he wouldn’t have been able to exacerbate the front-run sales that happened in that token and the complete loss of confidence in FTX as a custodian. It was a masterclass in financial chess playing.

Assessing The Murder

On some level, CZ had to have known what was going on at Alameda and by extension at FTX. It really wasn’t a secret that these people were doing really risky things. To find out how flimsy Sam’s understanding of DeFi actually seemed to be, all one has to do is listen to SBF’s appearance on the Odd Lots podcast from earlier this year. His rambling “money in a box” analogy is preposterous and isn’t really a framework for finding networks with actual value exchange. He’s essentially describing how yield farming, his firm’s bread and butter, is a Ponzi scheme without calling it that. CZ knew.

The cynic would probably say CZ planned this for quite some time. Going back to last year when Binance took its FTX investment exit, one many felt was premature, could CZ have already known how dangerous the FTX/Alameda relationship had become? Maybe. After all, CZ never sold the FTT that Binance controlled even when there couldn’t have been much of a reason to keep it as a utility token since CZ operates a competing exchange. CZ is probably a lot of things and like all humans is far from perfect. But I don’t think I can get there on the theory that FTX’s take down was planned as early as last year.

If Binance did end up acquiring what is left of FTX for the assets and the client list, I could probably get there. But Binance backed out of the deal. Unless he was able to unwind his entire FTT position in the open market, CZ probably lost money on this. I think the pin prick was more about CZ becoming irritated with SBF over a variety of things for quite some time. I don’t think he planned to take Sam out as part of his FTX exit from last year, but I do think he knew how risky FTX’s approach to the space had become.

I believe Changpeng Zhao connected some dots when CoinDesk released FTX’s leaked balance sheet. I won’t go as far as saying CZ is the hero that crypto needs, crypto doesn’t need one man to represent the entire space. That’s dangerous and we shouldn’t want that if we truly value decentralization. I think CZ is just an upper echelon strategist who took advantage of an opportunity to eliminate a key competitor and also take out a loud regulatory enemy all in one shot.

As for Sam, he’ll probably end up getting into politics. That’s clearly what he’s more interested in and he’ll probably fit right in. There’s something very icky about making a fortune pumping yield farm Ponzi-coins and then trying to use the regulators to ensure nobody else can do it after you. While orchestrating an 11-figure net worth is incredibly impressive, I don’t think SBF ever actually cared about the business he was in. Freedom from statists, decentralization, and peer-to-peer value exchange are ideals that he doesn’t seem to align with. He is profoundly at odds with the core ethos of the cypherpunks that created Bitcoin in the first place.

To me, this car is better off without SBF steering the wheel. I sincerely feel bad for anyone who has lost funds as a result of FTX’s collapse, but I’m glad Sam is gone.

Update 11/12: From Bad To Worse

If, like me, you thought this FTX meltdown saga was close to its conclusion with the announcement of Chapter 11 bankruptcy proceedings yesterday, boy was that wrong. Late last night ethscan sleuths monitoring FTX’s wallet addresses started to point out odd fund movements.

What made a lot of these moves particularly concerning was they weren’t strategic moves. In many cases, there was high slippage (fund loss) because of how quickly who ever did this was trying to do swaps at whatever rate he/she could get. On-chain analyst Foobar:

This is super sketchy, no liquidator would be taking actions like this

There was over $600 million in ETH tokens drained from FTX’s reserves last night and reportedly another $90 million in Solana that was swapped to ETH.

It seems a little over half of this outflow was taken by the “hacker” and the rest was quickly moved out by the team overseeing the liquidation. Ryne Miller is the General Counsel on the liquidation team and he acknowledged many of the funds that moved last night were not authorized transactions.

Soooo, that means they were stolen. And as one final “FU,” to customers, FTX’s app tried to push an app update that would have potentially installed a phishing attack that could have compromised private keys securing funds from self-custodial wallets. Despicable.

Interestingly, the normally chatty SBF was completely silent on Twitter last night while the remaining funds from his business were vanishing. CZ wasn’t silent though:

That’s one impressive “hacker.” This sure appears to be an inside job and if the authorities ever find Sam he’s probably in a lot of trouble. Stay safe out there, guys.